Annuity sales surge to $115B in Q2, with a new market leader, Wink reports

Annuity sales popped in the second quarter, Wink, Inc. reports, to nearly $115 billion – up 16.9% over Q1 and up 6.3% over the year-ago quarter.

Wink’s Sales & Market Report included 139 companies and included a shakeup at the top. Athene Annuity and Life Co. had been atop all annuity sales lists for several years and held 9.7% market share in Wink’s first-quarter report.

New York Life ranked as the No. 1 carrier overall for Q2 annuity sales, with a market share of 7.5%, Wink reported. Massachusetts Mutual Life Co. came in second place, while Athene, Corebridge Financial, and Equitable Financial completed the top five carriers in the market, respectively.

All annuities include the multi-year guaranteed annuity, traditional fixed annuity, indexed annuity, structured annuity, variable annuity, immediate income, and deferred income annuity product lines.

Total second-quarter sales for all deferred annuities were $111.5 billion, up 17.3% compared to the previous quarter and up 6.6% compared to the same period last year. All deferred annuities include the multiyear guaranteed annuity, traditional fixed, indexed annuity, structured annuity, and variable annuity product lines.

Noteworthy highlights for all deferred annuity sales in the second quarter include Athene USA ranking as the No. 1 carrier overall for deferred annuity sales, with a market share of 6.6%. Corebridge Financial moved into the second-ranked position, while MassMutual, New York Life, and Equitable Financial completed the top five carriers in the market, respectively.

MassMutual’s Stable Voya 3-Year, a MYG annuity, was the No. 1 selling deferred annuity, for all channels combined, in overall sales for the quarter.

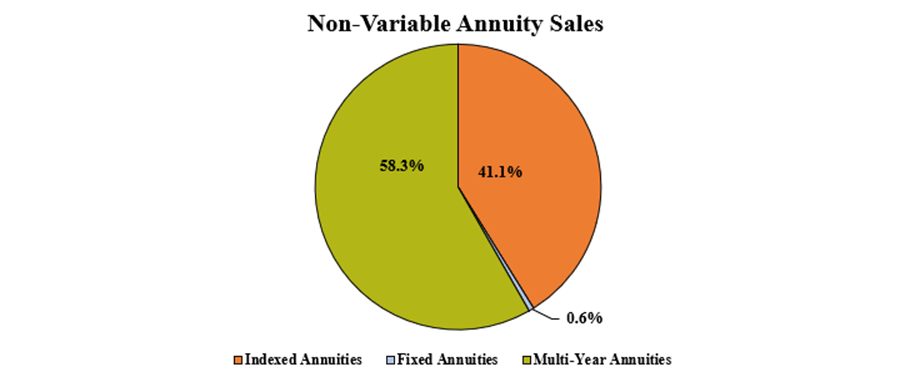

Total second-quarter non-variable deferred annuity sales were $77.9 billion, up 24.3% compared to the previous quarter and up 5.8% compared to the same period last year. Non-variable deferred annuities include the MYG annuity, traditional fixed annuity, and indexed annuity product lines.

Noteworthy highlights for non-variable deferred annuity sales in the second quarter include Athene ranking as the No. 1 carrier overall for non-variable deferred annuity sales, with a market share of 9.1%. MassMutual took the second-ranked position, while Corebridge Financial, New York Life, and Fidelity & Guaranty Life completed the top five carriers in the market, respectively.

Massachusetts Mutual Life’s Stable Voya 3-Year, a MYG annuity, was the No. 1 selling non-variable deferred annuity for the quarter, for all channels combined, in overall sales for the quarter.

Total second-quarter variable deferred annuity sales were $33.5 billion, up 3.8% compared to the previous quarter and up 8.4% compared to the same period last year. Variable deferred annuities include structured annuity and variable annuity product lines.

Noteworthy highlights for variable deferred annuity sales in the second quarter include Equitable Financial ranking as the No. 1 carrier overall for variable deferred annuity sales, with a market share of 16.6%. Jackson National Life continued in the second-place position, as Lincoln National Life, Allianz Life, and Brighthouse Financial completed the top five carriers in the market, respectively.

Equitable’s Structured Capital Strategies Plus 21, a structured annuity, was the No. 1 selling variable deferred annuity, for all channels combined, in overall sales for the fifth consecutive quarter.

Total second-quarter income annuity sales were $3.3 billion, up 4.6% compared to the previous quarter and down 1.3% compared to the same period last year. Income annuities include immediate income annuity and deferred income annuity product lines.

Noteworthy highlights for income annuity sales in the second quarter include New York Life ranking as the No. 1 carrier overall for income annuity sales, with a market share of 44.4%. MassMutual moved into the second-ranked position, as Western-Southern Life Assurance Company, Nationwide, and Penn Mutual completed the top five carriers in the market, respectively.

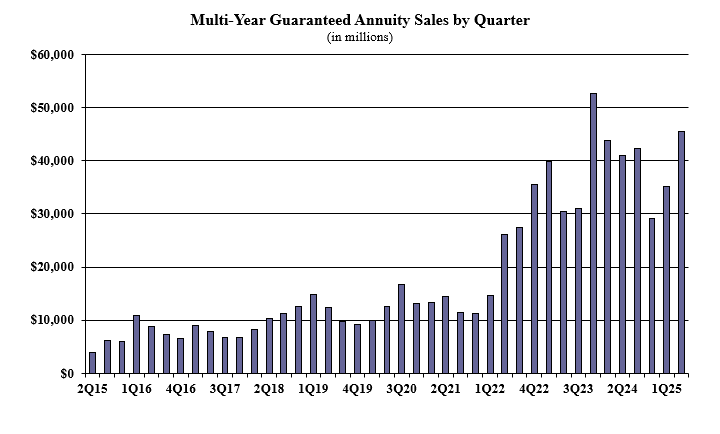

Multiyear guaranteed annuity sales in the second quarter were $45.4 billion, up 29.1% when compared to the previous quarter, and up 10.7% compared to the same period last year. MYGAs have a fixed rate that is guaranteed for more than one year.

Noteworthy highlights for MYGAs in the second quarter include MassMutual ranking as the No. 1 seller, with a market share of 13.3%. New York Life continued in the second-ranked position, while Corebridge Financial, Athene USA and Fidelity & Guaranty Life concluded as the top five carriers in the market, respectively. Massachusetts Mutual Life’s Stable Voya 3-Year product was the No. 1 selling multiyear guaranteed annuity for all channels combined.

“The banks and broker-dealers, in particular, are leading with MYGAs,” said Sheryl Moore, CEO of Wink, Inc., and Moore Market Intelligence.”As a result, two out of every five annuity sales are fixed annuities with a rate that is guaranteed for longer than one year.”

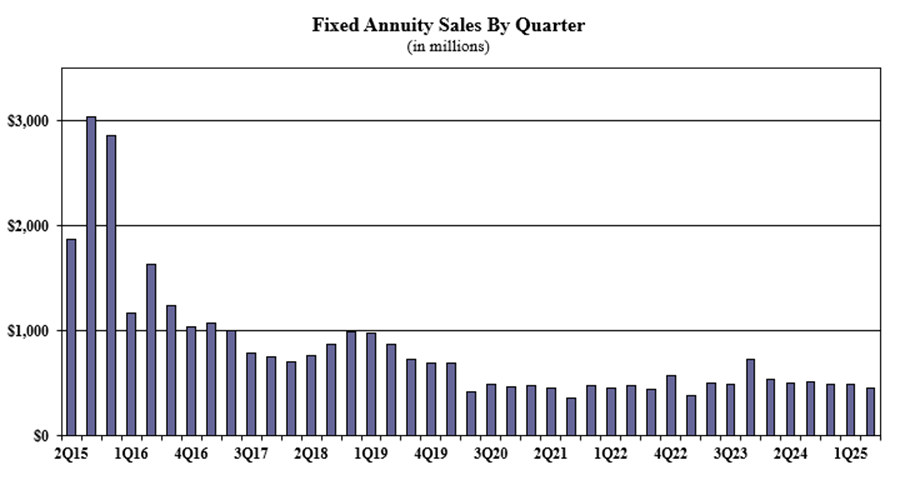

Traditional fixed annuity sales in the second quarter were $459.7 million, down 7.6% when compared to the previous quarter, and down 9.2% when compared with the same period last year. Traditional fixed annuities have a fixed rate that is guaranteed for one year only.

Noteworthy highlights for traditional fixed annuities in the second quarter include Global Atlantic Financial Group ranking as the No. 1 seller, with a market share of 18.4%. Modern Woodmen of America ranked second, while CNO Companies, National Life Group, and Western-Southern Life Assurance Company concluded as the top five carriers in the market, respectively. Forethought Life’s ForeCare Fixed Annuity was the No. 1 selling fixed annuity, for all channels combined, for the twentieth consecutive quarter.

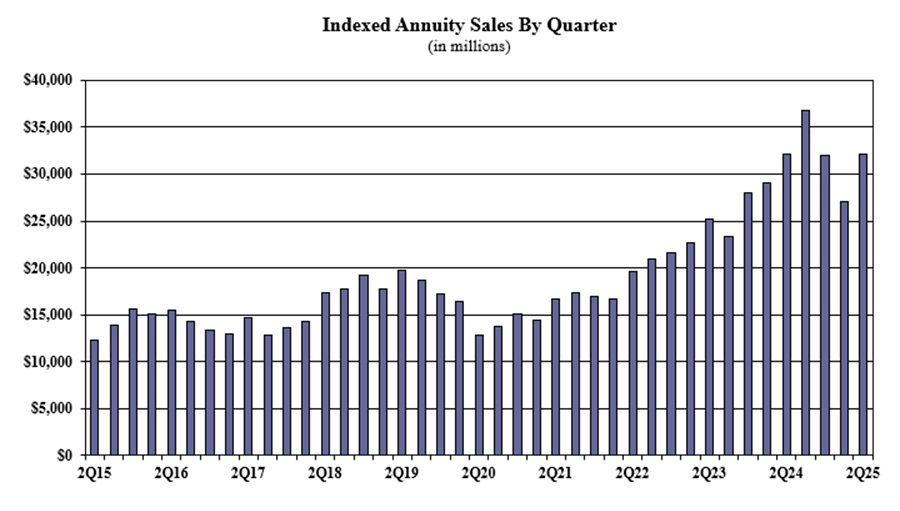

Indexed annuity sales for the second quarter were $32 billion, up 18.6% compared to the previous quarter, and down 0.1% compared with the same period last year. Indexed annuities have a floor of no less than zero percent and limited excess interest that is determined by the performance of an external index, such as the S&P 500.

Noteworthy highlights for indexed annuities in the second quarter include Athene USA ranking as the No. 1 seller, with a market share of 12.6%. Corebridge Financial ranked second, while Allianz Life, Sammons Financial Companies, and American Equity Companies completed the top five carriers in the market, respectively. American Equity’s IncomeShield 10 was the No. 1 selling indexed annuity, for all channels combined, for the third consecutive quarter.

Structured annuity sales in the second quarter were $18.2 billion, up 10.8% compared to the previous quarter, and up 16.2% compared to the same period last year. It was a record-setting quarter for structured annuity sales. Structured annuities have a limited negative floor and limited excess interest that is determined by the performance of an external index or subaccounts.

Noteworthy highlights for structured annuities in the second quarter include Equitable Financial ranking as the No. 1 seller, with a market share of 20.7%. Allianz Life ranked second, while Brighthouse Financial, Prudential, and Lincoln National Life completed the top five carriers in the market, respectively. Equitable’s Structured Capital Strategies Plus 21 was the No. 1 selling structured annuity, for all channels combined, for the fifth consecutive quarter.

“What amazed me about structured annuities this quarter was a relatively new entrant that had already moved into the top ten rankings for the product,” Moore said. “A long-time variable annuity seller, who held off on their structured design, is poised to crush it.”

Variable annuity sales in the second quarter were $15.3 billion, down 3.3% compared to the previous quarter, and up 0.4% compared to the same period last year. Variable annuities have no floor, and the potential for gains/losses is determined by the performance of subaccounts that may be invested in an external index, stocks, bonds, commodities, or other investments.

Noteworthy highlights for variable annuities in the second quarter include Jackson National Life ranking as the No. 1 seller, with a market share of 19.1%. Equitable Financial ranked second, while New York Life, Nationwide, and Lincoln National Life finished as the top five carriers in the market, respectively. Jackson National’s Perspective II Flexible Premium Variable & Fixed Deferred Annuity was the No. 1 selling variable annuity for the twenty-fifth consecutive quarter, for all channels combined.

“As long as the market keeps trending up, we should see VA sales increase over last year,” explained Moore.

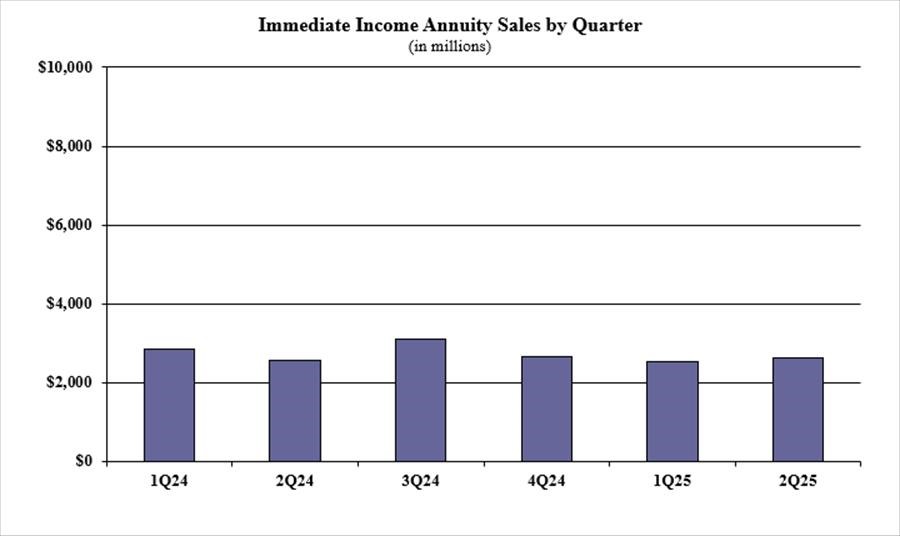

Immediate income annuity sales in the second quarter were $2.6 billion, up 4.6% compared to the previous quarter and up 3.2% compared to the same period last year.

Noteworthy highlights for income annuities in the second quarter include New York Life ranking as the No. 1 seller, with a market share of 43.8%. Western-Southern Life Assurance Company ranked second, while MassMutual, Nationwide, and Penn Mutual finished as the top five carriers in the market, respectively.

Deferred income annuity sales in the second quarter were $701.3 million, up 4.3% compared to the previous quarter and down 15.5% compared to the same period last year.

Noteworthy highlights for DIAs in the second quarter include New York Life ranking as the No. 1 seller, with a market share of 46.6%. MassMutual ranked second, as Western-Southern Life Assurance Company, Integrity Life Companies, and Global Atlantic Financial Group finished as the top five carriers in the market, respectively.

Wink now reports sales on all annuity lines of business, as well as all life insurance product lines, Moore noted.

The post Annuity sales surge to $115B in Q2, with a new market leader, Wink reports appeared first on Insurance News | InsuranceNewsNet.