Variable annuity sales surge as market confidence remains high, Wink finds

Annuity buyers continued to show faith in the market as 2025 came to a close, with traditional variable and structured annuity sales up significantly, Wink Inc. reported.

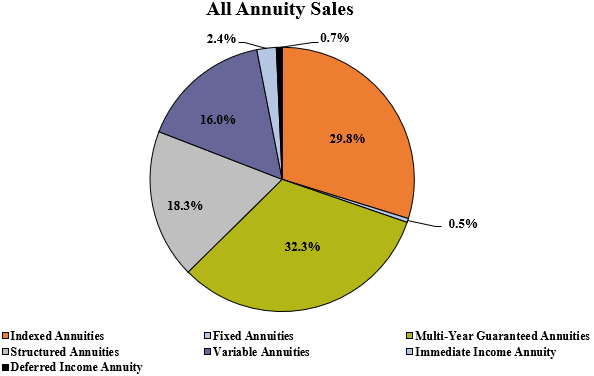

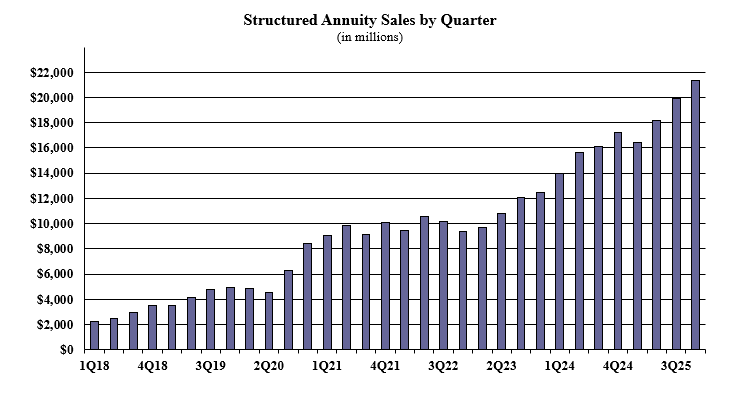

Structured annuities, also known as registered index-linked or RILAs, recorded $21.3 billion in Q4 sales, up 7% compared to the third quarter and up 23.8% compared to the year-ago quarter, Wink found.

Structured annuities allow investors to participate in stock market gains (up to a cap) while providing a “safety net” against losses through buffers or floors.

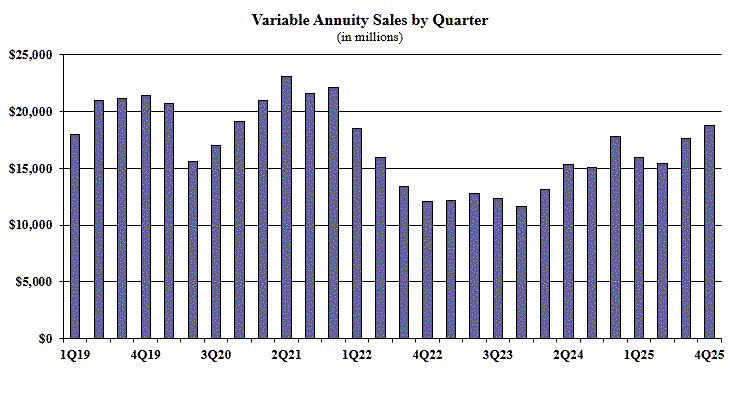

Variable annuity sales in the fourth quarter were $18.7 billion, up 6.6% as compared to the previous quarter, and up 5.3% compared to the same period last year, Wink reported. Total 2025 variable annuity sales were $67.6 billion.

Total fourth quarter sales for all annuities were $116.9 billion, down 0.6% when compared to the previous quarter and up 16.7% when compared to the same period last year. Total 2025 sales for all annuities were $448.9 billion. Since Wink began tracking sales of all annuities, it marked a record-setting year, topping the prior 2024 record by 4.9%.

All annuities include the multi-year guaranteed annuity, traditional fixed annuity, indexed annuity, structured annuity, variable annuity, immediate income annuity and deferred income annuity product lines.

Noteworthy highlights for all annuity sales in the fourth quarter include Athene USA ranking as the No. 1 carrier overall for annuity sales, with a market share of 6.7%. Massachusetts Mutual Life Companies came in second place, while Jackson National Life, Nationwide, and Allianz Life completed the top five carriers in the market, respectively.

The full Wink report:

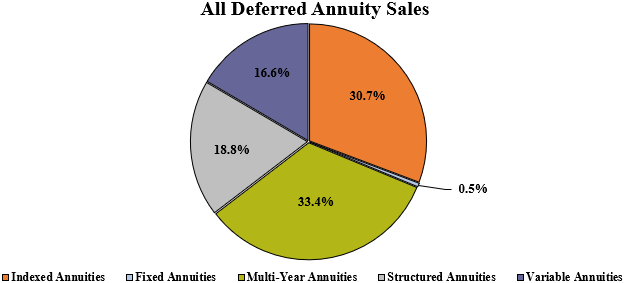

Total fourth quarter sales for all deferred annuities were $113.3 billion, down 0.4% compared to the previous quarter and up 17.3% compared to the same period last year. Total 2025 deferred annuity sales were $434.9 billion. This was a record-setting year for deferred annuity sales, topping the prior 2024 record by 5.3%.

All deferred annuities include the multi-year guaranteed annuity, traditional fixed, indexed annuity, structured annuity and variable annuity product lines.

Noteworthy highlights for all deferred annuity sales in the fourth quarter include Athene USA ranking as the No. 1 carrier overall for deferred annuity sales, with a market share of 6.9%. Jackson National Life moved into the second-ranked position, while Massachusetts Mutual Life Companies, Nationwide, and Allianz Life completed the top five carriers in the market, respectively.

Massachusetts Mutual Life’s Stable Voyage 3-Year, a MYG annuity, was the No. 1 selling deferred annuity, for all channels combined, for the quarter.

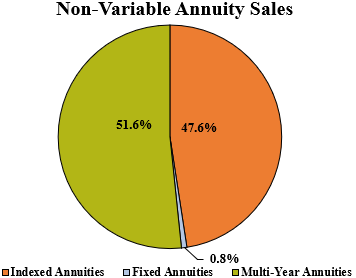

Total fourth quarter non-variable deferred annuity sales were $73.2 billion, down 4% when compared to the previous quarter and up 18.9% compared to the same period last year. Total 2025 non-variable deferred annuity sales were $291.3 billion. This was a record-setting year for deferred non-variable annuity sales, topping the prior 2024 record by 0.9%. Non-variable deferred annuities include the MYG annuity, traditional fixed annuity, and indexed annuity product lines.

Noteworthy highlights for non-variable deferred annuity sales in the fourth quarter include Athene USA ranking as the No. 1 carrier overall for non-variable deferred annuity sales, with a market share of 10.1%. Massachusetts Mutual Life Companies took the second-ranked position, while Corebridge Financial, Nationwide, and Allianz Life completed the top five carriers in the market, respectively.

Massachusetts Mutual Life’s Stable Voyage 3-Year, a MYG annuity, was the No. 1 selling non-variable deferred annuity, for all channels combined, for the quarter.

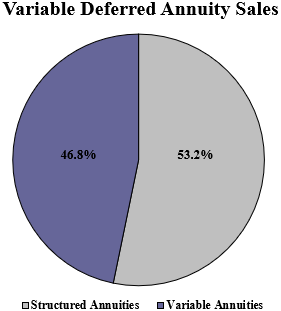

Total fourth quarter variable deferred annuity sales were $40.1 billion, up 6.8% when compared

to the previous quarter and up 14.4% when compared to the same period last year. Total 2025 variable deferred annuity sales were $143.6 billion. Variable deferred annuities include structured annuity and variable annuity product lines.

Noteworthy highlights for variable deferred annuity sales in the fourth quarter include Jackson National Life ranking as the No. 1 carrier overall for variable deferred annuity sales, with a market share of 16.3%. Equitable Financial continued in the second-place position, as Lincoln National Life, Allianz Life, and Nationwide completed the top five carriers in the market, respectively.

Jackson National’s Perspective II Flexible Premium Variable & Fixed Deferred Annuity, a variable annuity, was the No. 1 selling variable deferred annuity, for all channels combined, for the second consecutive quarter.

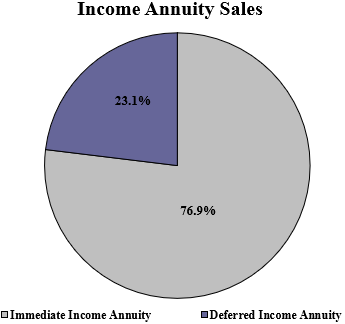

Total fourth quarter income annuity sales were $3.6 billion, down 6% when compared to the previous quarter and up 1.3% compared to the same period last year. Total 2025 income annuity sales were $13.9 billion. Income annuities include immediate income annuity and deferred income annuity product lines.

Noteworthy highlights for income annuity sales in the fourth quarter include New York Life ranking as the No. 1 carrier overall for income annuity sales, with a market share of 41.9%. Massachusetts Mutual Life Companies continued in the second-ranked position, as Western-Southern Life Assurance Company, Nationwide, and American National completed the top five carriers in the market, respectively.

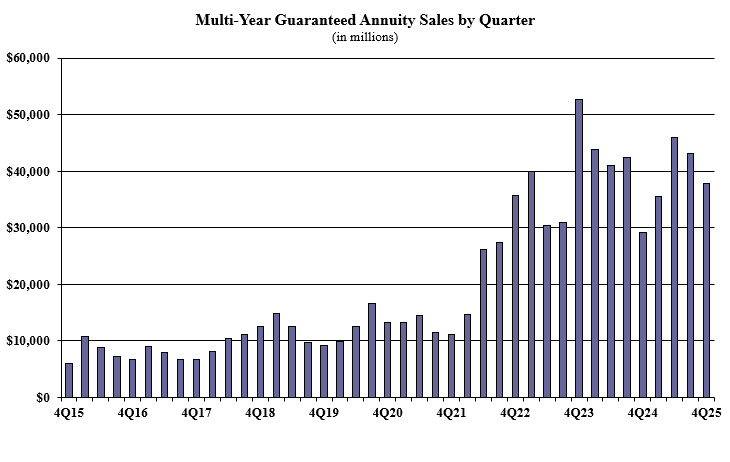

Multi-year guaranteed annuity sales in the fourth quarter were $37.8 billion, down 12.1% compared to the previous quarter, and up 29.9% compared to the same period last year. Total 2025 MYGA sales were $162.5 billion. MYGAs have a fixed rate that is guaranteed for more than one year.

Noteworthy highlights for MYGAs in the fourth quarter include Massachusetts Mutual Life Companies ranking as the No. 1 seller, with a market share of 13.6%. Athene USA moved into the second-ranked position, while New York Life, Nationwide, and Corebridge Financial concluded the top five carriers in the market, respectively. Massachusetts Mutual Life’s Stable Voyage 3-Year product was the No. 1 selling multi-year guaranteed annuity, for all channels combined, for the quarter.

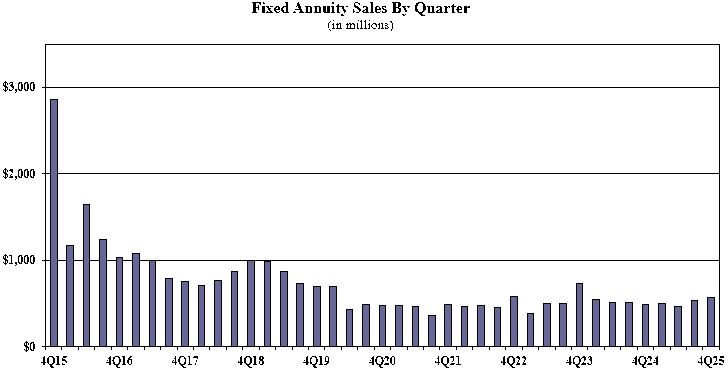

Traditional fixed annuity sales in the fourth quarter were $574.5 million, up 6.7% compared to the previous quarter, and up 16.9% compared with the same period last year. Total 2025 traditional fixed annuity sales were $2 billion. Traditional fixed annuities have a fixed rate that is guaranteed for one year only.

Noteworthy highlights for traditional fixed annuities in the fourth quarter include Global Atlantic Financial Group ranking as the No. 1 seller, with a market share of 16.5%. Equitable Financial ranked second, while CL Life, Nationwide, and CNO Companies concluded the top five carriers in the market, respectively. Forethought Life’s ForeCare Fixed Annuity was the No. 1 selling fixed annuity, for all channels combined, for the twenty-second consecutive quarter.

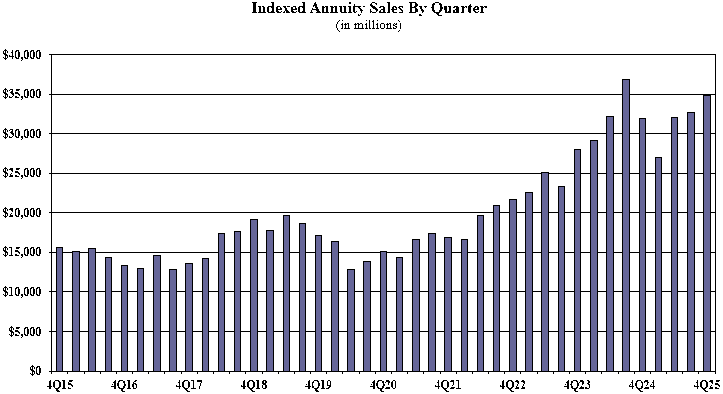

Indexed annuity sales for the fourth quarter were $34.8 billion, up 6.4% compared to the

previous quarter, and up 8.9% compared with the same period last year. Total 2025 indexed annuity sales were $126.7 billion. Indexed annuities have a floor of no less than zero percent and limited excess interest that is determined by the performance of an external index, such as S&P 500.

Noteworthy highlights for indexed annuities in the fourth quarter include Athene USA ranking as the No. 1 seller, with a market share of 10.4%. Allianz Life ranked second, while Corebridge Financial, Delaware Life, and Sammons Financial Companies completed the top five carriers in the market, respectively. Allianz Life’s Allianz Benefit Control+ Annuity was the No. 1 selling indexed annuity, for all channels combined, for the quarter.

Sheryl Moore, CEO of both Wink, Inc., and Moore Market Intelligence said: “This was the second-highest quarter ever for indexed annuity sales; 3Q24 was too tough to be beat. When you consider the recent volatility in the markets, I am anticipating that both indexed and structured annuities will continue to gain favor in 2026.”

Structured annuity sales in the fourth quarter were $21.3 billion, up 7% compared to the previous quarter, and up 23.8% compared to the same period last year. This was a record-setting quarter for structured annuity sales, topping the prior third quarter 2025 record by 7%.

Total 2025 structured annuity sales were $75.9 billion. This was also a record-setting year for structured annuity sales, topping the prior 2024 record by 20.6%.

Noteworthy highlights for structured annuities in the fourth quarter include Equitable Financial ranking as the No. 1 seller, with a market share of 19.6%. Allianz Life ranked second, while Jackson National Life, Brighthouse Financial, and Lincoln National Life completed the top five carriers in the market, respectively. Equitable’s Structured Capital Strategies Plus 21 was the No. 1 selling structured annuity, for all channels combined, for the seventh consecutive quarter.

“The top variable annuity seller has been steadily increasing their structured annuity sales,” Moore said. “It will be interesting to see if this company defends its structured annuity market share, similar to their VA strategy.”

Variable annuity sales in the fourth quarter were $18.7 billion, up 6.6% as compared to the previous quarter, and up 5.3% compared to the same period last year. Total 2025 variable annuity sales were $67.6 billion. Variable annuities have no floor, and the potential for gains/losses is determined by the performance of subaccounts that may be invested in an external index, stocks, bonds, commodities, or other investments.

Noteworthy highlights for variable annuities in the fourth quarter include Jackson National Life ranking as the No. 1 seller, with a market share of 22.8%. Nationwide ranked second, while Equitable Financial, Lincoln National Life, and New York Life finished as the top five carriers in the market, respectively.

Jackson National’s Perspective II Flexible Premium Variable & Fixed Deferred Annuity was the No. 1 selling variable annuity for the twenty-seventh consecutive quarter, for all channels combined.

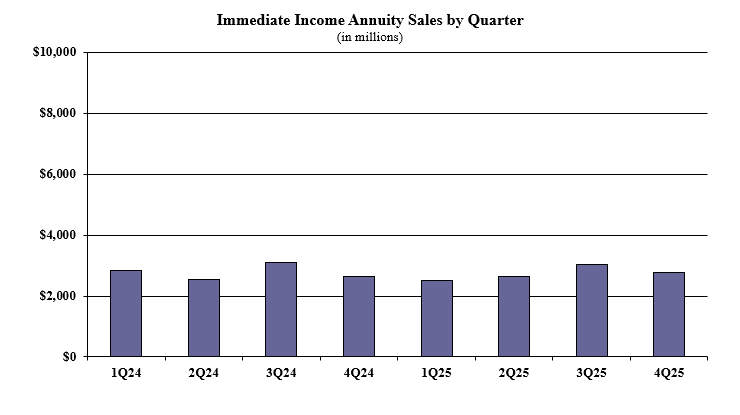

Immediate income annuity (single-premium income annuities) sales in the fourth quarter were $2.7 billion, down 8.6% compared to the previous quarter and up 5% compared to the same period last year. Total 2025 SPIA sales were $10.9 billion.

Noteworthy highlights for SPIAs in the fourth quarter include New York Life ranking as the No. 1 seller, with a market share of 43.5%. Massachusetts Mutual Life Companies ranked second, while Nationwide, Western-Southern Life Assurance Company, and American National finished as the top five carriers in the market, respectively.

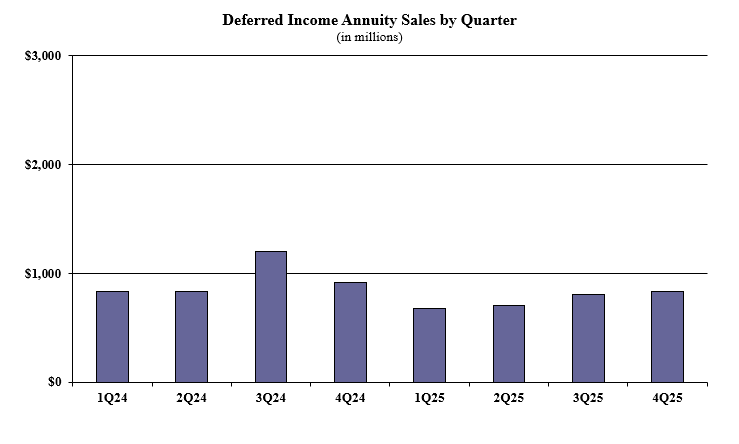

Deferred income annuity sales in the fourth quarter were $832.8 million, up 3.8% compared to the previous quarter and down 9.1% compared to the same period last year. Total 2025 DIA sales were $3 billion.

Noteworthy highlights for DIAs in the fourth quarter include New York Life ranking as the No. 1 seller, with a market share of 36.4%. Massachusetts Mutual Life Companies ranked second, as Western-Southern Life Assurance Company, Integrity Life Companies, and Corebridge Financial finished as the top five carriers in the market, respectively.

Wink reports sales on all annuity lines of business, as well as all life insurance product lines.

The post Variable annuity sales surge as market confidence remains high, Wink finds appeared first on Insurance News | InsuranceNewsNet.