Life insurers post modest gains following record 2024, S&P Global finds

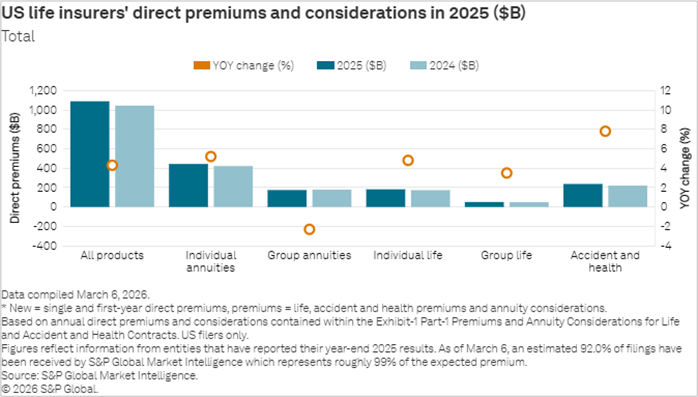

According to S&P Global Market Intelligence, the life insurance industry experienced a 4.3% increase in total direct premiums and considerations in 2025, reaching a record high of $1.09 trillion.

Those numbers are striking when compared to the 14.6% rise in 2024, which was the most rapid expansion in two decades.

The analysis examined individual and group life insurance and annuities, as well as accident and health insurance. Individual life premiums saw a 4.8% growth, driven by select products rather than a broad-based increase. Variable life direct premiums surged by 41.9%, but contributed only 1.4% to the individual life total. Indexed individual life premiums increased by 10.7%, accounting for 13.2% of the total.

Individual annuity direct premiums grew by less than 5.2% in 2025, a fraction of the 21.2% expansion rate in the prior year.

Direct premiums in accident and health increased by 7.8%, down from a 10.3% growth rate in 2024. Private participation in government programs like Medicare and Medicaid fueled expansion, while traditional group benefits products saw modest growth of less than 4% in disability income and dental insurance lines.

Group annuities saw the lone year-over-year decline of 2.3%. This largely reflects the impact of jumbo pension risk transfer group annuity placements in the first quarter of 2024.

Powerful 2024 annuity sales

In 2024, individual annuities took off due to a combination of demographics and market conditions, according to Tim Zawacki, principal analyst, S&P Global Market Intelligence.

“In September of that year, the Federal Reserve lowered interest rates by 50 basis points, driving growth for the industry,” he explained. “It was also a record year for pension risk transfers with jumbo transactions turbo charging the industry’s growth.”

As a result of more annuity products and carriers in the market, the individual annuity market racked up record sales in the last several years. Many consumers purchased annuities with 3- to 5-year terms, which will be ending soon.

“If long-term rates remain elevated, consumers will likely invest this money back into annuities,” Zawacki said.

“The insurance industry (which includes individual annuities) provides strategies to manage wealth and provide principal protection,” Zawacki added. “While the pandemic had an initial effect, today life insurance growth is largely driven by tax incentives.”

The current market conditions lend themselves to an increase in the industry, particularly in the annuity space, he said.

When it comes to life insurance, Zawacki noted that the middle market is under a lot of economic pressure given the high cost of groceries, gas, food, housing costs and other daily expenses.

“Younger people are under a lot of stress with rising home costs and student loan debt. There is a tendency among this group to view life insurance as a discretionary expense and it’s a tough environment for discretionary expenses,” he added.

“Despite this, life insurance products are well-positioned for growth, particularly among the mass affluent who are looking for tax gains. The industry, however, needs to look at how to attract younger consumers.”

What will the future hold for the industry?

“Looking ahead, as long as there isn’t a recession or a spike in unemployment, the dynamics are favorable for the industry to see continued growth in the mid-single digits,” Zawacki said.

Demographics are impacting the industry’s growth with more people in their 50s and 60s making it an attractive environment for retirement savings products.

“It all comes down to supply and demand, which has remained consistent over the last few years,” Zawacki said. “Middle market consumers are struggling while the mass affluent are looking for attractive rates with principal protection.”

The post Life insurers post modest gains following record 2024, S&P Global finds appeared first on Insurance News | InsuranceNewsNet.

")