‘I get confused:’ Regulators ponder increasing illustration complexities

The path to changes to rules governing life insurance and annuity illustrations is sure to be a long one. Regulators took another step Tuesday with a review of initial comment letters on the topic.

The new Life Insurance and Annuities Illustrations Working Group, established by the National Association of Insurance Commissioners, held its second call to discuss the 11 comment letters it received and posted to its website. The group first met in February.

Letter writers included Dick Weber, an industry veteran who participated in the long process to develop a life insurance illustration regulation in 1995, and Scott Stolz, who noted he has four decades in the annuity industry and owns four annuities.

Regulators, actuaries and consumer advocates also weighed in.

“I am an insurance attorney and have been for almost 20 years, and I get confused by these illustrations,” said Matt Gendron is acting deputy director and general counsel for the Rhode Island Department of Business Regulation. “I’m not quite sure I follow them. That’s probably an issue.”

Regulators highlighted examples of annuity illustrations suggesting annual returns between 10% and 27%, prompting questions about whether consumers are receiving an accurate picture of potential performance at the point of sale.

“The original objective for illustrations … was for the consumer to understand how the policy works,” Weber recalled. “And what we observed is that both agents and consumers routinely use the policy illustration to form an expectation of what is likely to occur, and that’s exactly not what any of us want.”

Concerns over consumer understanding

Several commenters stressed that current illustrations may be misused or misunderstood, despite longstanding rules that prohibit them from being treated as performance projections.

In its letter, the American Academy of Actuaries said illustrations were designed to demonstrate how products function under certain scenarios — not to predict returns. Attempting to use them as forward-looking performance indicators could mislead consumers, said Donna Megregian, chairperson of the AAA’s Life Products Committee.

“We do understand that illustrations are poor predictors of performance because they were never meant to be performance indicators or projections,” she added. “The regulations avoided using these words in the definitions of an illustration.”

Consumer advocates echoed those concerns, arguing that complex, lengthy illustrations — often spanning dozens of pages — can overwhelm buyers and lead to unrealistic expectations. Birny Birnbaum, executive director of the Center for Economic Justice, called for eliminating projected returns entirely and instead focusing on simplified explanations of how products operate under different market conditions.

“This is the most important reform,” Birnbaum stressed. “Providing projections for purposes of income planning or investment planning requires the expertise of advisors trained in financial planning, and should be done by a financial planning professional, not within an illustration.”

Other comments identified several structural features within current illustration frameworks that can contribute to higher depicted returns.

CANNEX outlined factors such as renewal rate assumptions, selection of favorable historical periods and inconsistencies between current strategy rates and the economic environment of the illustrated scenarios. Together, these elements can skew illustrated outcomes upward, particularly during strong market cycles.

Proposed solutions included requiring disclosures about the risk of lower renewal rates, adding alternative scenarios with reduced returns and modernizing how scenarios are generated—potentially moving away from historical back-testing toward forward-looking models.

“A very simple fix would be to not allow for any back tested data,” Stolz said. “It has to be actual index performance, to the extent that there needs to be something illustrated for a certain time period on a new index that’s introduced.”

Existing regs debated

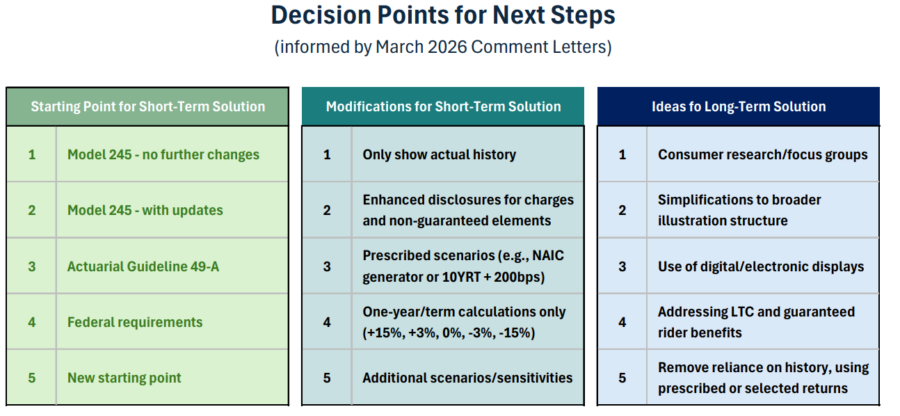

A central question in the discussion was whether to build on existing rules — particularly Model Regulation 245, which governs annuity illustrations — or pursue a more comprehensive overhaul.

Some industry groups support broader adoption of the current model across states as a near-term step to improve consistency.

Others, including several regulators and consumer advocates, argued that the model is outdated and insufficient to address current concerns. They called for more fundamental changes, including limits on the use of historical data, clearer disclosures of non-guaranteed elements and greater use of visual tools to improve consumer understanding.

Regulators are considering a two-track approach: a short-term effort to address the most pressing concerns, potentially within a year, explained Chairman Ben Slutsker, director of life actuarial valuation at the Minnesota Department of Commerce, or a longer-term review of broader structural reforms.

The working group is also expected to examine real-world illustrations from states that have adopted current rules compared with those that have not, in an effort to evaluate their effectiveness.

The working group concluded with plans for a second 45-day exposure period to collect more comments on the path forward.

© Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

The post ‘I get confused:’ Regulators ponder increasing illustration complexities appeared first on Insurance News | InsuranceNewsNet.