Advantage Capital signed an agreement with global investment manager Oaktree Capital Management to provide critical funding support for its financially troubled life insurance subsidiaries.

The firm known as A-Cap announced the deal Friday for Oaktree to acquire a controlling stake in Atlantic Coast Life Insurance Co., while also providing capital to Sentinel Security Life Insurance Co.

Oaktree will fund a “surplus note investment into a newly created captive insurance company,” the new partners explained in a news release.

A-Cap battled state regulators and AM Best in recent years over the financial strength of Atlantic Coast and Sentinel Security. On Jan. 23, AM Best downgraded the financial strength ratings of both insurers. In 2024, A-Cap sued AM Best over a proposed ratings downgrade – a lawsuit later settled.

Kenneth King, chairman and CEO of A-Cap, stressed Oaktree’s “track record of investing alongside insurers, particularly during times of transition.

“Oaktree’s insurance-focused credit expertise and flexible, long-term capital will support disciplined growth of our balance sheet, enhance our asset liability profile, and strengthen our ability to serve our policyholders and distribution partners over the long term,” he added in a news release.

All of the net proceeds from the transactions will be used to “support the growth and long-term objectives of Sentinel and its policyholders,” the release said.

“The company will benefit from our meaningful experience in regulated carve-outs as it works to complete its pre-closing transaction milestones,” said Patrick C. George, senior vice president, global opportunities, at Oaktree. “Following closing, we believe both Atlantic Coast Life and Sentinel will be well positioned to prioritize policyholder protection, financial strength, and sustainable long-term growth.”

Oaktree is a global investment manager specializing in alternative investments, with $223 billion in assets under management as of Dec. 31, 2025. The firm “emphasizes an opportunistic, value-oriented, and risk-controlled approach to investments in credit, equity, and real estate,” the release said.

Financial strength questioned

AM Best said its ratings downgrade is “based on weakness in A-CAP Group’s business profile as manifested in the material decrease in new premium and material increase in surrenders/outflows, as well as reputational damage resulting from publicized regulatory rulings.”

Regulators argued A-Cap used flawed, internal valuations to overstate the worth of high-risk assets, while independent audits valued those same assets at significantly lower amounts. While the states banned the insurers from writing new business, administrative law judges in both states later stayed or overturned these orders.

A-Cap provided information that “demonstrates surrenders and outflows have decreased,” AM Best noted. The insurers’ primary focus is the fixed index annuity market, a “dynamic and credit sensitive sector with strong long-term prospects,” the ratings agency added.

AM Best downgraded the FSR from B++ (Good) to B (Fair) and the Long-Term Issuer Credit Rating from “bbb” (Good) to “bb+” (Fair) for both A-Cap life insurers.

“The downgrades are also based on a decline in AM Best’s overall assessment of A-CAP Group’s balance sheet strength,” the release added. “AM Best acknowledges A-CAP Group’s pending capital raise, but also recognizes its level of illiquid assets, concentrated reinsurance leverage, which is mitigated through the use of funds held and modified coinsurance agreements, along with a recent decline in its overall capital adequacy ratios that have not fully recovered to historic levels.”

A group of large PHL Variable policyholders, and the Connecticut insurance commissioner both took aim at Nassau Financial Group in separate court filings this week.

Both the policyholders and interim Commissioner Joshua Hershman, serving as the rehabilitator in the proposed liquidation of the financially troubled PHL, are after the same thing: Money.

Hundreds of millions of dollars are at stake as Connecticut regulators navigate the liquidation proposed by Hershman on Dec. 31, 2025. State Superior Court Judge Daniel J. Klau approved rehabilitation for PHL in May 2024.

Since then, Judge Klau has ruled on several twists and turns in the case. Former insurance commissioner Andrew Mais steadfastly pursued a rehabilitation plan before retiring in late November 2025. Hershman abruptly pivoted to liquidation in a Dec. 31 status report.

That ratcheted up the pressure to find an equitable financial solution. Particularly for so-called “over-the-cap” policyholders, who are entitled to death benefits in excess of $300,000, a moratorium was established by a June 2024 court order. That figure mirrors state guaranty association limits.

A group of over-the-cap policyholders filed a motion Tuesday to obtain “relief” allowing the group to pursue “certain claims against Nassau Financial Group (and related subsidiaries), Golden Gate Capital and others … for looting PHL at the expense of the” policyholders.

The group alleged self-dealing, breach of fiduciary duty, fraudulent and negligent misrepresentation, state unfair trade and insurance violations, and civil Racketeer Influenced and Corrupt Organizations Act violations.

‘Facilitate an orderly transition’

Over-the-cap policyholders “will pursue these tort claims on a fully contingent basis that will be accretive to PHL in rehabilitation and facilitate an orderly transition from rehabilitation to liquidation,” their motion reads.

Meanwhile, Hershman filed a status update on Tuesday. In it, he provided more details of claims against Nassau and Golden Gate hinted at in the Dec. 31 report.

Affiliates of Nassau Financial provide administrative services to the rehabilitator under agreements that precede the rehabilitation proceeding. From May 2024 through December 2025, Nassau charged the PHL companies $10.7 million for investment services and $65.6 million for administrative services.

“There are pending disputes between Nassau and the Rehabilitator concerning these arrangements and charges assessed under the agreements,” Hershman wrote. “The Rehabilitator believes that the charges … have been and continue to be materially above market as a result of the allocation of certain expenses to PHL. Nassau disputes this.”

As of the end of 2025, there are about 8,000 active universal life insurance policies, with about 3,200 having death benefits greater than the applicable state guaranty association limits, the status report said.

Of those, 343 of the active over-the-cap UL policies “appear to be owned by institutional investors,” Hershman wrote, which represents 26% of the total outstanding death benefits on the policies.

Additional policyholder claims

In a memorandum supporting their filing, the over-the-cap policyholders also alleged that the court-appointed rehabilitator has failed to aggressively pursue claims against Nassau and Golden Gate despite acknowledging that potential claims against the companies may exist.

They further claim the rehabilitator may have a conflict of interest because some of the transactions now under scrutiny were previously approved by state regulators.

Nassau Financial Group (then Nassau Re) acquired PHL Variable as part of a 2016 purchase of The Phoenix Companies for $217.2 million.

The over-the-cap policyholders say that PHL was weakened through complex reinsurance arrangements involving affiliated entities, including transactions with captive insurers and offshore reinsurers.

“Almost immediately following the acquisition, PHL was systematically gutted by Nassau and its affiliates and rendered hopelessly insolvent,” the policyholders’ memo reads. “Billions in sham, circular, non-arm’s length reinsurance transactions were consummated by and among various PHL and Nassau affiliates and captive insurance companies located in Connecticut, Vermont and the Cayman Islands.”

According to the policyholders, those transactions allowed affiliated companies to replace assets on PHL’s balance sheet with obligations from related entities, while the insurer took credit for billions of dollars in reserve relief.

The policyholders also pointed to litigation in Delaware involving alleged stranger-originated life insurance transactions that they say raised additional concerns about dealings involving Nassau-affiliated entities.

If granted permission to intervene, the policyholders argued that any recoveries could ultimately benefit the rehabilitation estate while allowing policyholders to seek damages for losses above guaranty association limits.

The policyholders asked the court to schedule a hearing on the request as soon as possible.

Advancements in technology are ushering in what experts on a recent InsTech panel have dubbed the “golden age of underwriting,” a period expected to be marked by greater speed, efficiency and managing general agency activity.

“I think now, with the evolution of technology, that we can move into this golden age because the technology allows, especially underwriters, to have systems that they can use and be effective with,” Matthew Twist, chief risk officer and commercial director at Concirrus, said during the webinar.

However, he underscored that the industry hasn’t hit that golden peak just yet, noting that there are still more challenges to address before insurance can get there.

“If we’re going to talk about the golden age of underwriting, we must be realistic about where we are today. And if we’re in an industry where very skilled and capable people are keying in information into a system and then into another system and potentially another system after that, are we really in the golden age? Probably not,” he said.

His fellow panelists agreed and emphasized the need for dialogue between IT and underwriters in the field to ensure technology is not only developed in a meaningful way but also that uptake is encouraged on an individual level.

Underwriting transformed

One of the biggest ways technology can transform underwriting for the better is by making the process faster, smoother and more efficient overall, panelists said.

“Insurance, on the whole, is still quite an admin-heavy industry. Tech is essential for us to free up our time and do exactly what we need to be doing, which is building our client base, building our relationships and fundamentally underwriting,” Lisa Rowe, senior underwriter, financial lines and cyber, Specialty MGA UK, said.

At the same time, she said consultation between tech teams and end users — which she suggested “has been missing a lot of the time” — is crucial for implementation and adoption.

“I’m sure we’ve all been in a position where a new tech stack has been implemented and we’re going into it saying, ‘This doesn’t really do what I need it to do.’ I think embracing technology but also consulting with the end user is going to bring forward a more golden age, as it were,” she said.

Rowe acknowledged, however, that underwriters can also do a better job of adapting to new technologies and strategies.

“I think it’s a two-pronged conversation. Some of us can adapt to change a little bit more readily than others; some underwriters are still quite old school — they like paper. So, there’s a bit of a shift needed to a degree from the individuals,” she said.

Some of this is already happening, as business user engagements are “at an all-time high,” according to Robin Merttens, chairman and co-founder, InsTech.

“I’ve not seen this level of genuine interest from underwriters, brokers or accounting teams. That’s partly because there’s a sort of age profile — the tech savviness is improving, so that people know what tech can do, they’re using it more in their personal lives and they get involved,” Merttens said.

More tech-driven MGA activity

Merttens also pointed to the potential for greater MGA activity resulting from innovators taking advantage of the tech momentum to build a fully digital, AI-enabled business.

Twist agreed, noting that it could be “quite an appealing option” for an entrepreneurial underwriter stuck in “more of a legacy setup.”

“We see a massive rise in the MGA market, in the London market specifically and across the US. And, arguably, in the next three to five years, these are the companies that will be successful because they’re set up for success immediately,” Twist said.

Piers Williams, CRO, Diesta, added that the delegated market has been growing consistently year on year, creating ripe conditions for MGA growth.

“If we look at also the cycles that we often see in insurance, we’ve seen a lot of those mid and larger-sized MGAs be consolidated over the last few years… We are certainly seeing there is this new wave of startup MGAs looking at these very specific or far more tailored and customer-centric products in the market, using technology to back up those offerings, both from an underwriting side and also right across that organization’s architecture and utilization of technology,” Williams said.

No gold medal yet

While prospects are improving, Rowe agreed with Twist’s point that the insurance industry hasn’t reached its golden age of technology just yet and still must contend with managing risks alongside benefits.

“There’s a way to go, but we are moving forward in a positive light in terms of our adoption of tech and AI. The golden age of underwriting is coming. It’s going to take a concerted effort for us all to work together to achieve that, but we’re in an increasingly competitive environment and adopting, as opposed to running away from, these types of tech enablements will be the decisive factor for success,” Rowe said.

InsTech is a UK-based global data insights company and insurance community founded in 1971

Concirrus is an AI-powered underwriting platform founded in 2012.

Diesta is an AI-driven insurtech startup founded in 2022 that specializes in automation of premium reconciliation and distribution.

Specialty MGA UK is part of the MNK Group, a global reinsurer founded in 2009.

Younger generations are going through serious health issues earlier in life, with substantial implications for employer-sponsored health plans. That was the word from UnitedHealthcare and Health Action Council, which published a white paper on their findings.

The report pointed out that costs for employer-sponsored health care benefits are rising more quickly than general inflation and wage growth, affecting employers and their employees. For example, the report said, KFF’s 2025 Employer Health Benefits Survey reports a 6% increase in per-employee benefit costs in 2025, with a projected 6.5% rise in 2026. These trends reflect the continued affordability pressures facing the American health system.

“Employers are seeing health issues show up earlier and feeling the cost impact sooner,” said Patty Starr, president and CEO of Health Action Council. “This report gives plan sponsors the transparency and insight they need to spot health problems earlier, help people stay on top of basic and preventive care, and help them stay healthier while keeping benefits affordable.”

Main takeaways from the report

One of the main takeaways of the report is that health risks and health care costs are showing up earlier than many employers expect, putting added pressure on employer‑sponsored health plans, said Craig Kurtzweil, chief data analytics officer for UnitedHealthcare Employer & Individual. “Costs for employer‑sponsored health care benefits continue to rise faster than general inflation and wage growth, affecting both employers and their employees,” he added.

That cost pressure is being driven in part by an increase in serious, high‑cost health events, Kurtzweil explained. Conditions such as heart attacks, strokes, complex surgeries and illnesses such as cancer or genetic disorders are becoming more common across the workforce. In fact, Kurtzweil said, “these major health events are now about twice as frequent as they were five years ago, and average monthly claims tied to them have increased nearly 40% since 2020.”

At the same time, the report points to a clear generational shift. Although millennials and Generation Z still have lower overall health care claims than those of older generations, costs for these younger generations are rising at a much faster pace, Kurtzweil added. Between 2023 and 2025, their year‑over‑year growth rate was nearly double that of baby boomers. “The data shows younger adults are developing chronic conditions such as diabetes, obesity and high blood pressure earlier in life and are less likely to engage in regular primary care, which increases the likelihood that health issues become more serious and more costly over time,” he said.

Taken together, Kurtzweil said, these trends suggest that some longstanding assumptions about how age, risk and cost show up in employer health plans are shifting. “For employers, and for the agents and advisors who support them, the report underscores the importance of paying closer attention to emerging risks earlier and across a broader portion of the workforce,” he added.

Using the report’s data

Employers can play an important role by using insights about their workforce to shape benefits and engagement strategies more intentionally, Kurtzweil said.

To start, the data can help employers better understand the specific health risks within their employee population and focus on earlier intervention. “Encouraging preventive care and consistent use of primary care is especially important,” Kurtzweil pointed out. “The report finds that people who regularly see a primary care provider have 27% lower claims for major health events, along with fewer emergency room visits and hospital admissions.”

Beyond primary care, Kurtzweil said, employers can also look at benefit design that makes care easier to understand and easier to access. Plans that offer clearer upfront costs and simpler navigation can help employees make more informed decisions about where to go for care and when.

Finally, Kurtzweil said, the report highlights how evidence‑based programs such as metabolic health support, lifestyle coaching and weight management can help reinforce care outside the doctor’s office when paired with strong primary care engagement. “Using data to identify early warning signs, including gaps in preventive care or early indicators of chronic conditions, can help employers step in sooner, before those issues turn into higher‑cost health events,” he added.

Overall, Kurtzweil said, “the report shows that when employers act on these insights and focus on early engagement, preventive care, and primary care access, they can help support better employee health while helping to manage long‑term health care costs.”

Access the white paper (pdf) for strategies to help improve workforce health engagement and affordability.

The Department of Labor said in court documents this week that it supports a district court motion to vacate its Retirement Security Rule, the department’s most recent attempt to extend fiduciary duty.

The motion was filed jointly with a group of industry trade groups that initially filed a lawsuit to prevent the RSR from taking effect. With both sides now on the same side, the motion to vacate likely means the end of the Biden-era RSR.

Since 2015, the DOL has made multiple efforts to expand the definition of “fiduciary” under the Employee Retirement Income Security Act of 1974, aiming to require that financial professionals who give retirement advice — including brokers, agents and insurance sellers — put clients’ best interests first.

In April 2016, the DOL finalized a broad fiduciary rule set to apply in 2017, but that rule was vacated in 2018 by a federal appeals court, which said the agency had exceeded its authority.

In April 2024, under a new administration, the DOL issued another rule — dubbed the Retirement Security Rule — again expanding the fiduciary definition to include many more retirement-investment advisors and amending prohibited-transaction exemptions.

The rule was slated to take effect in September 2024. However, legal challenges quickly followed. In July 2024, a federal judge issued a nationwide stay, blocking implementation while the lawsuit proceeds — meaning the expanded fiduciary obligations are on hold for now.

Annuity buyers continued to show faith in the market as 2025 came to a close, with traditional variable and structured annuity sales up significantly, Wink Inc. reported.

Structured annuities allow investors to participate in stock market gains (up to a cap) while providing a “safety net” against losses through buffers or floors.

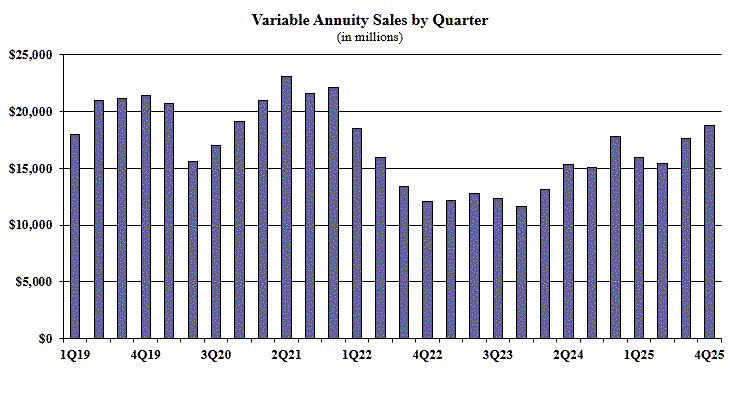

Variable annuity sales in the fourth quarter were $18.7 billion, up 6.6% as compared to the previous quarter, and up 5.3% compared to the same period last year, Wink reported. Total 2025 variable annuity sales were $67.6 billion.

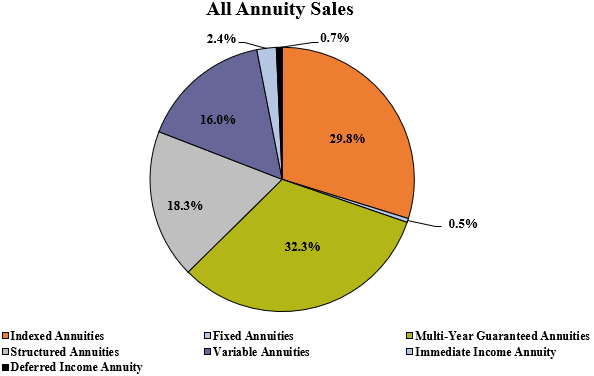

Total fourth quarter sales for all annuities were $116.9 billion, down 0.6% when compared to the previous quarter and up 16.7% when compared to the same period last year. Total 2025 sales for all annuities were $448.9 billion. Since Wink began tracking sales of all annuities, it marked a record-setting year, topping the prior 2024 record by 4.9%.

All annuities include the multi-year guaranteed annuity, traditional fixed annuity, indexed annuity, structured annuity, variable annuity, immediate income annuity and deferred income annuity product lines.

Noteworthy highlights for all annuity sales in the fourth quarter include Athene USA ranking as the No. 1 carrier overall for annuity sales, with a market share of 6.7%. Massachusetts Mutual Life Companies came in second place, while Jackson National Life, Nationwide, and Allianz Life completed the top five carriers in the market, respectively.

The full Wink report:

Courtesy of Wink, Inc.

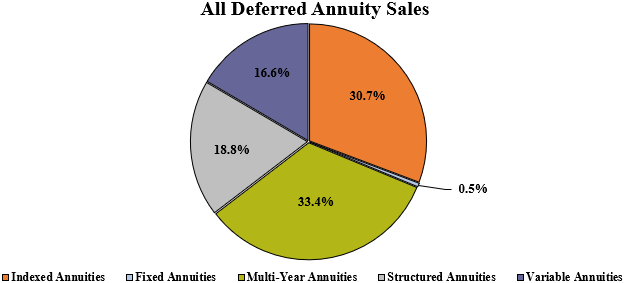

Total fourth quarter sales for all deferred annuities were $113.3 billion, down 0.4% compared to the previous quarter and up 17.3% compared to the same period last year. Total 2025 deferred annuity sales were $434.9 billion. This was a record-setting year for deferred annuity sales, topping the prior 2024 record by 5.3%.

All deferred annuities include the multi-year guaranteed annuity, traditional fixed, indexed annuity, structured annuity and variable annuity product lines.

Noteworthy highlights for all deferred annuity sales in the fourth quarter include Athene USA ranking as the No. 1 carrier overall for deferred annuity sales, with a market share of 6.9%. Jackson National Life moved into the second-ranked position, while Massachusetts Mutual Life Companies, Nationwide, and Allianz Life completed the top five carriers in the market, respectively.

Massachusetts Mutual Life’s Stable Voyage 3-Year, a MYG annuity, was the No. 1 selling deferred annuity, for all channels combined, for the quarter.

Courtesy of Wink, Inc.

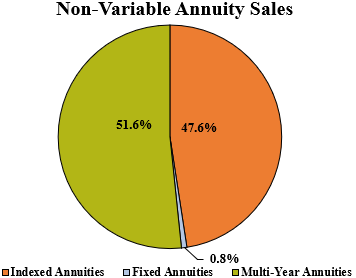

Total fourth quarter non-variable deferred annuity sales were $73.2 billion, down 4% when compared to the previous quarter and up 18.9% compared to the same period last year. Total 2025 non-variable deferred annuity sales were $291.3 billion. This was a record-setting year for deferred non-variable annuity sales, topping the prior 2024 record by 0.9%. Non-variable deferred annuities include the MYG annuity, traditional fixed annuity, and indexed annuity product lines.

Noteworthy highlights for non-variable deferred annuity sales in the fourth quarter include Athene USA ranking as the No. 1 carrier overall for non-variable deferred annuity sales, with a market share of 10.1%. Massachusetts Mutual Life Companies took the second-ranked position, while Corebridge Financial, Nationwide, and Allianz Life completed the top five carriers in the market, respectively.

Massachusetts Mutual Life’s Stable Voyage 3-Year, a MYG annuity, was the No. 1 selling non-variable deferred annuity, for all channels combined, for the quarter.

Courtesy of Wink, Inc.

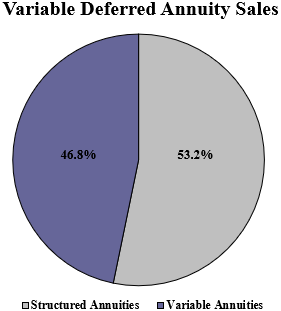

Total fourth quarter variable deferred annuity sales were $40.1 billion, up 6.8% when compared

to the previous quarter and up 14.4% when compared to the same period last year. Total 2025 variable deferred annuity sales were $143.6 billion. Variable deferred annuities include structured annuity and variable annuity product lines.

Noteworthy highlights for variable deferred annuity sales in the fourth quarter include Jackson National Life ranking as the No. 1 carrier overall for variable deferred annuity sales, with a market share of 16.3%. Equitable Financial continued in the second-place position, as Lincoln National Life, Allianz Life, and Nationwide completed the top five carriers in the market, respectively.

Jackson National’s Perspective II Flexible Premium Variable & Fixed Deferred Annuity, a variable annuity, was the No. 1 selling variable deferred annuity, for all channels combined, for the second consecutive quarter.

Courtesy of Wink, Inc.

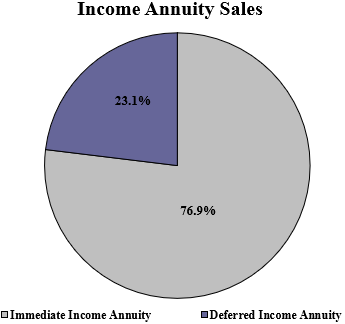

Total fourth quarter income annuity sales were $3.6 billion, down 6% when compared to the previous quarter and up 1.3% compared to the same period last year. Total 2025 income annuity sales were $13.9 billion. Income annuities include immediate income annuity and deferred income annuity product lines.

Noteworthy highlights for income annuity sales in the fourth quarter include New York Life ranking as the No. 1 carrier overall for income annuity sales, with a market share of 41.9%. Massachusetts Mutual Life Companies continued in the second-ranked position, as Western-Southern Life Assurance Company, Nationwide, and American National completed the top five carriers in the market, respectively.

Courtesy of Wink, Inc.

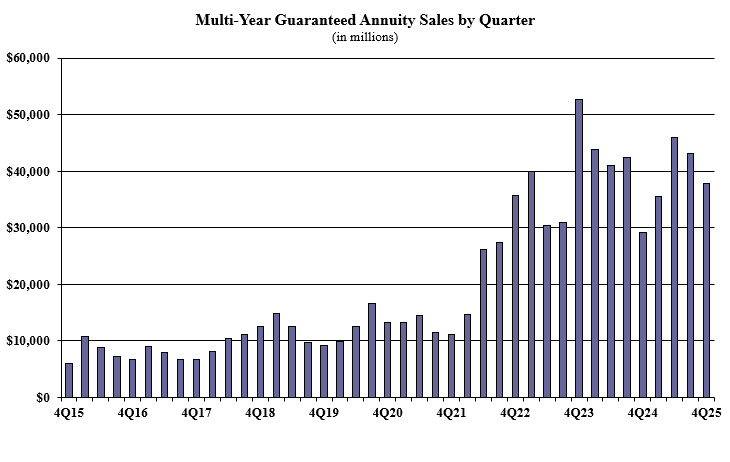

Multi-year guaranteed annuity sales in the fourth quarter were $37.8 billion, down 12.1% compared to the previous quarter, and up 29.9% compared to the same period last year. Total 2025 MYGA sales were $162.5 billion. MYGAs have a fixed rate that is guaranteed for more than one year.

Noteworthy highlights for MYGAs in the fourth quarter include Massachusetts Mutual Life Companies ranking as the No. 1 seller, with a market share of 13.6%. Athene USA moved into the second-ranked position, while New York Life, Nationwide, and Corebridge Financial concluded the top five carriers in the market, respectively. Massachusetts Mutual Life’s Stable Voyage 3-Year product was the No. 1 selling multi-year guaranteed annuity, for all channels combined, for the quarter.

Courtesy of Wink, Inc.

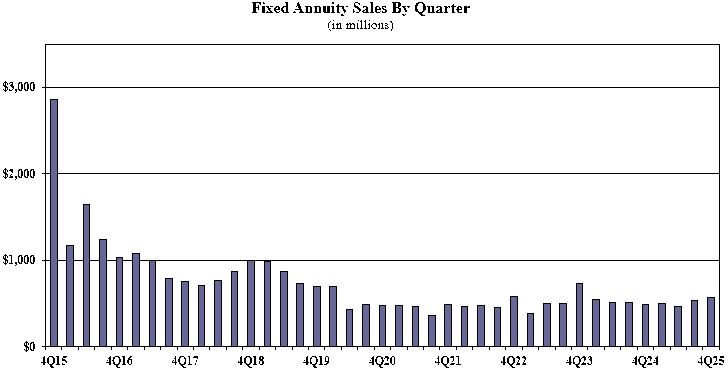

Traditional fixed annuity sales in the fourth quarter were $574.5 million, up 6.7% compared to the previous quarter, and up 16.9% compared with the same period last year. Total 2025 traditional fixed annuity sales were $2 billion. Traditional fixed annuities have a fixed rate that is guaranteed for one year only.

Noteworthy highlights for traditional fixed annuities in the fourth quarter include Global Atlantic Financial Group ranking as the No. 1 seller, with a market share of 16.5%. Equitable Financial ranked second, while CL Life, Nationwide, and CNO Companies concluded the top five carriers in the market, respectively. Forethought Life’s ForeCare Fixed Annuity was the No. 1 selling fixed annuity, for all channels combined, for the twenty-second consecutive quarter.

Courtesy of Wink, Inc.

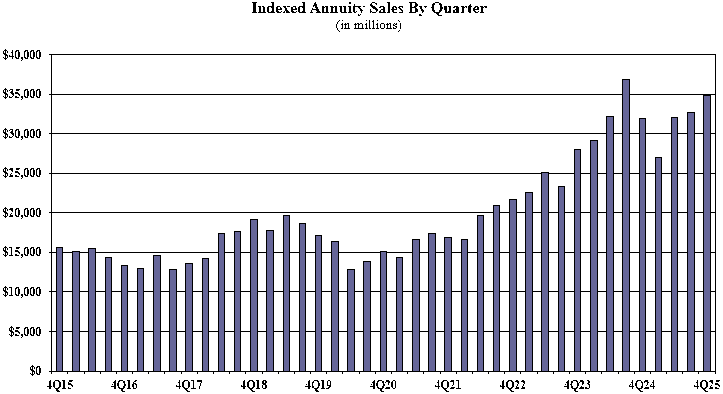

Indexed annuity sales for the fourth quarter were $34.8 billion, up 6.4% compared to the

previous quarter, and up 8.9% compared with the same period last year. Total 2025 indexed annuity sales were $126.7 billion. Indexed annuities have a floor of no less than zero percent and limited excess interest that is determined by the performance of an external index, such as S&P 500.

Noteworthy highlights for indexed annuities in the fourth quarter include Athene USA ranking as the No. 1 seller, with a market share of 10.4%. Allianz Life ranked second, while Corebridge Financial, Delaware Life, and Sammons Financial Companies completed the top five carriers in the market, respectively. Allianz Life’s Allianz Benefit Control+ Annuity was the No. 1 selling indexed annuity, for all channels combined, for the quarter.

Sheryl Moore, CEO of both Wink, Inc., and Moore Market Intelligence said: “This was the second-highest quarter ever for indexed annuity sales; 3Q24 was too tough to be beat. When you consider the recent volatility in the markets, I am anticipating that both indexed and structured annuities will continue to gain favor in 2026.”

Courtesy of Wink, Inc.

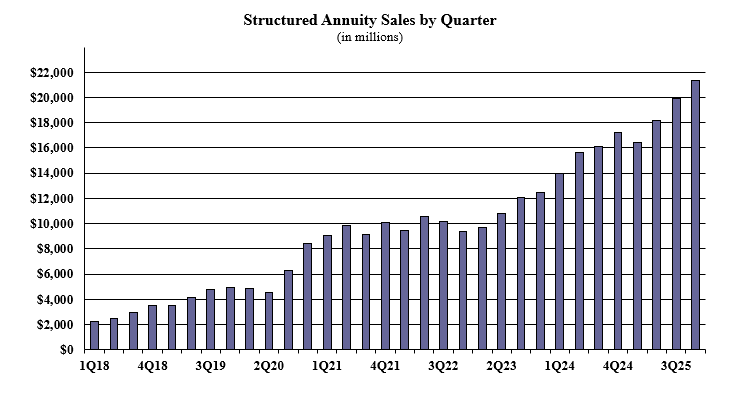

Structured annuity sales in the fourth quarter were $21.3 billion, up 7% compared to the previous quarter, and up 23.8% compared to the same period last year. This was a record-setting quarter for structured annuity sales, topping the prior third quarter 2025 record by 7%.

Total 2025 structured annuity sales were $75.9 billion. This was also a record-setting year for structured annuity sales, topping the prior 2024 record by 20.6%.

Noteworthy highlights for structured annuities in the fourth quarter include Equitable Financial ranking as the No. 1 seller, with a market share of 19.6%. Allianz Life ranked second, while Jackson National Life, Brighthouse Financial, and Lincoln National Life completed the top five carriers in the market, respectively. Equitable’s Structured Capital Strategies Plus 21 was the No. 1 selling structured annuity, for all channels combined, for the seventh consecutive quarter.

“The top variable annuity seller has been steadily increasing their structured annuity sales,” Moore said. “It will be interesting to see if this company defends its structured annuity market share, similar to their VA strategy.”

Courtesy of Wink, Inc.

Variable annuity sales in the fourth quarter were $18.7 billion, up 6.6% as compared to the previous quarter, and up 5.3% compared to the same period last year. Total 2025 variable annuity sales were $67.6 billion. Variable annuities have no floor, and the potential for gains/losses is determined by the performance of subaccounts that may be invested in an external index, stocks, bonds, commodities, or other investments.

Noteworthy highlights for variable annuities in the fourth quarter include Jackson National Life ranking as the No. 1 seller, with a market share of 22.8%. Nationwide ranked second, while Equitable Financial, Lincoln National Life, and New York Life finished as the top five carriers in the market, respectively.

Jackson National’s Perspective II Flexible Premium Variable & Fixed Deferred Annuity was the No. 1 selling variable annuity for the twenty-seventh consecutive quarter, for all channels combined.

Courtesy of Wink, Inc.

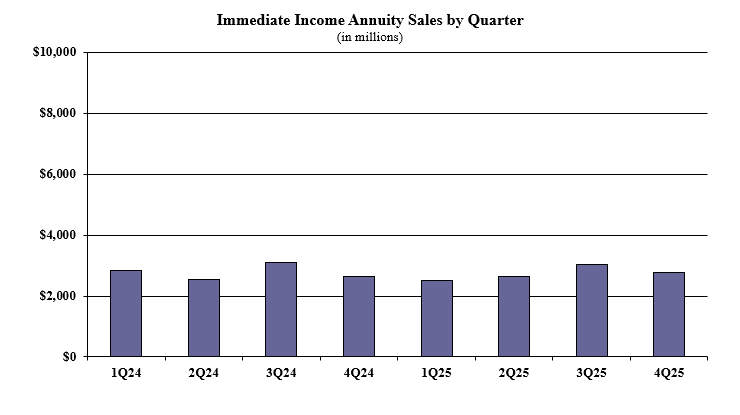

Immediate income annuity (single-premium income annuities) sales in the fourth quarter were $2.7 billion, down 8.6% compared to the previous quarter and up 5% compared to the same period last year. Total 2025 SPIA sales were $10.9 billion.

Noteworthy highlights for SPIAs in the fourth quarter include New York Life ranking as the No. 1 seller, with a market share of 43.5%. Massachusetts Mutual Life Companies ranked second, while Nationwide, Western-Southern Life Assurance Company, and American National finished as the top five carriers in the market, respectively.

Courtesy of Wink, Inc.

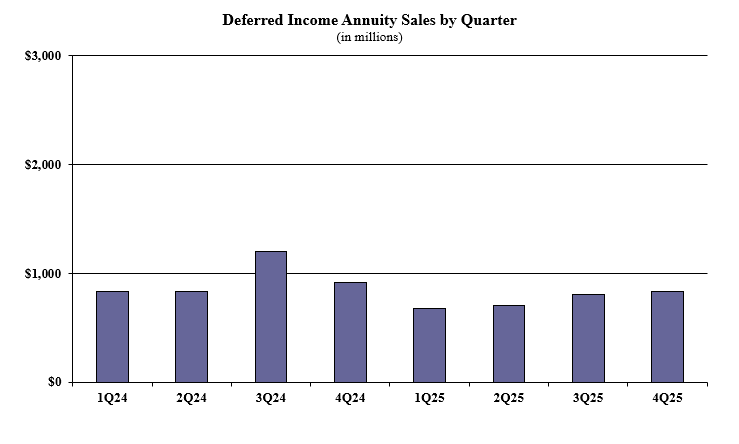

Deferred income annuity sales in the fourth quarter were $832.8 million, up 3.8% compared to the previous quarter and down 9.1% compared to the same period last year. Total 2025 DIA sales were $3 billion.

Noteworthy highlights for DIAs in the fourth quarter include New York Life ranking as the No. 1 seller, with a market share of 36.4%. Massachusetts Mutual Life Companies ranked second, as Western-Southern Life Assurance Company, Integrity Life Companies, and Corebridge Financial finished as the top five carriers in the market, respectively.

Courtesy of Wink, Inc.

Wink reports sales on all annuity lines of business, as well as all life insurance product lines.

At the end of February, the Securities and Exchange Commission’s (SEC) Division of Enforcement announced important updates to its Enforcement Manual.

These changes were ultimately made to improve the consistency and uniformity of investigative practices, the agency said, allowing for a more efficient process.

The manual, which was last updated in 2017, will now be reviewed annually to ensure it aligns with the SEC’s mission to protect investors, maintain market integrity, and support capital formation.

According to Rami Sneineh, vice president of Insurance Navy Brokers, updating the Enforcement Manual each year is a major step towards more adaptive and modern government regulation.

“Every day, I see how outdated rules harm the very people they are designed to protect,” Sneineh said. “Market inefficiency caused by a slow regulatory system can be a real problem. Bringing uniformity to the Wells process ensures that all advisors receive equal treatment, regardless of which regional office is handling their case.”

The SEC “Wells process” is a formal procedure that allows individuals or entities under investigation by the SEC to present their side of the story before the agency decides whether to file enforcement charges.

How the SEC’s updates impact insurance advisors and clients

These updates will primarily affect insurance advisors in how they document and assess the rationale for their client recommendations.

“The SEC’s shift towards a more formalized approach to investigations indicates a stronger focus on written evidence of the advisory decision-making process,” said Joe Braier, president and CEO of Lake Country Advisors.

Advisors who can clearly demonstrate they have documented their clients’ objectives, the suitability of the products they recommended, and the transparency in compensation will be better positioned to navigate the evolving regulatory landscape.

On the other hand, advisors whose practices rely on disorganized records and informal rationales may face greater scrutiny.

“The standardized investigative procedures will quickly identify inconsistencies in these practices, making them more transparent in the new enforcement environment,” Braier explained.

These changes not only affect insurance advisors but will also significantly impact the financial customers or clients they serve. As advisors adopt a more transparent, disciplined approach, clients can expect clearer communication and more thorough analysis, the SEC said.

This increased transparency should set them up to make smarter, more strategic decisions and foster a trustworthy, meaningful relationship with their advisors.

Best practices for advisors adapting to these updates

As an insurance advisor, it’s important to view regulatory documentation as an advisory service rather than a compliance hassle, experts say.

For every recommendation, advisors recommend documenting it in writing to help tie together the client’s goals, products chosen, and compensation terms in one document.

“Well-documented records will ultimately produce a narrative, which will support the professional judgment of the advisor in the event of any subsequent inquiry,” Braier said.

Having a well-organized filing system typically resolves regulatory investigations before they turn into formal investigations.

“Based on my years of experience in the field, I’ve found that proactive compliance is always more cost-effective than dealing with a litigation case,” Sneineh said. “It enables you to integrate these standards into the everyday operations of your business, making it more resilient and ultimately more valuable over time.”

The potential for artificial intelligence to transform underwriting workflows has caught up to the surety bonding industry. But it has also led to concerns about job security as a new survey by Lance Surety Bonds found 41% of surety professionals are worried about roles being replaced.

“It’s really a combination of concerns. There’s the obvious one of AI replacing jobs, but there’s also uncertainty around what happens when technology becomes the main decision maker,” Eric Weisbrot, digital marketing manager, Lance Surety Bonds, said.

He noted that alongside concern about job loss, many insurance professionals are “concerned about “overreliance on the technology and the lack of clear accountability if something goes wrong.”

In his view, the underlying issue is more about humans being removed from the loop and AI overshadowing human judgement.

“Once underwriting decisions start relying heavily on algorithms, questions about transparency and bias quickly follow. The real fear is not just job loss, but losing human judgment in the decision-making process. When real financial consequences are involved, that concern is understandable,” Weisbrot said.

However, the survey emphasized that AI itself is not the enemy. In fact, three out of five bonding professionals said they have already implemented automation in their bonding process and most said it can positively impact their roles.

As such, Weisbrot said balance between workflow modernization and workforce upskilling is key to navigating this new normal.

The case for modernization

Lance Surety Bonds’ survey confirmed what many industry leaders have already warned —- companies no longer have the luxury of avoiding AI in an era with increasing demand for technology-driven solutions.

“What’s important to keep in mind is that client demands are evolving faster than ever,” Weisbrot said. “Fifty-six percent of surety bond pros are saying it’s becoming more common for their clients to expect a digital-first experience. While that’s certainly an emerging trend in surety bonds, it’s really a trend happening across all types of insurance products.”

Surety bonding and risk management professionals surveyed also expressed confidence in AI’s capabilities, with 43% trusting it to be more accurate than traditional models, 58% saying they believe it can enhance underwriting roles and 66% saying going digital is key to staying competitive.

However, at the same time, one in five surety bonding professionals said their work is still manual — and most believe it’s causing their company to lose business. Fifty-nine percent of respondents said their firms are “losing money and speed because these more ‘old-school’ methods, like paper or fax, can be costly and time-consuming.”

Meanwhile, 70% of small owners surveyed said they would defect from their current surety bond provider “immediately” if they could get bonded in less than 10 minutes using AI instead.

“In an era where speed is crucial and businesses are having to do less with more, every second seems to count,” Weisbrot said.

Outpacing human skill

Concern about job loss is one of the potential downsides of AI being perceived as so effective, as indicated by the results of the study.

“If AI is already earning that trust and getting buy-in to outperform human judgment on assessing risk, one of the core skills of underwriters and advisors, then these roles built around human evaluation and processing are certainly feeling the pressure,” Weisbrot explained.

However, he believes the risk isn’t a simple matter of mass redundancy but a more nuanced concern about role transformation. While the term “skills gap” never appears in the research, he believes the results imply this could be a potential factor at play.

“The concerns around overreliance on algorithms and a lack of transparency in AI decisions signal that while some are adopting these tools, they still don’t fully understand them, which is a skills gap in itself,” Weisbrot said.

“Half of those we surveyed admitted they feel pressured to modernize, whether it’s due to competition from insurtech firms or internal bottlenecks. The pressure without capability is the perfect environment for a skills gap to take hold.”

Technological balance

The solution lies in integrating new technology while advancing AI literacy, according to Weisbrot, who emphasized that outdated workflows are costing companies who choose to do nothing.

“While leaders should invest in AI tools, you must invest in actual training as well; you can’t just integrate these new tools and expect your team to ‘figure it out.’ Build your staff and their confidence up by allowing them to upskill or train on these new technologies, and you should see an increased confidence in interpreting, auditing, and overriding AI decisions,” he said.

But individual professionals also have a role to play, he added, in learning to work with technology rather than fear it or see it as competition.

“Our research suggests pros best positioned for success are ones who can work alongside AI rather than go head-to-head with it. Combine speed and efficiency from these tools with your relationship management, ethical judgement and contextual knowledge that algorithms can’t replicate,” Weisbrot said.

Lance Surety Bonds is a U.S.-based surety bond provider founded in 2010 and based out of Doylestown, PA. Its study, “The Future of Surety Bonds: Will AI and Automation Change the Industry?” was conducted in June 2025, surveying 544 Americans working in roles related to surety bonding and risk management.

Earlier this year, a new law went into effect in Texas, requiring insurers to provide a reason for declining or canceling an auto or homeowners policy.

HB 2067 applies to decisions made by insurance companies after January 1, 2026, and affects all property and casualty insurers, including farm mutual insurance companies.

According to Carol Sherron, senior vice president and southwest zone client advisory leader at Marsh, a global professional services firm, this law marks a significant step toward greater transparency in the insurance marketplace.

“Making it standard practice for insurers to share this information benefits consumers by giving them clear insight into the factors influencing coverage decisions,” Sherron explained.

What HB 2067 means for consumers

The transparency of HB 2067 allows consumers to take targeted actions that address their unique concerns and improve their risk profiles. This can, in turn, expand their options for insurance coverage.

“Most A-rated carriers that we work with at Marsh are already sharing rationale for their decisions,” Sherron said. “However, this new ruling requiring all carriers to do so is a step in the right direction for standardized consumer transparency.”

Of course, there is a downside in the form of an administrative burden placed on carriers that are required to meet these reporting requirements, as well as on the Texas Department of Insurance, which must collect, review, and publish the information.

Ways to communicate this law to clients

For insurance agents, HB 2067 underscores the importance of proactive communication with clients regarding underwriting concerns and risk management.

“Normalizing these discussions and providing education focused on improving insurability empowers clients to make educated decisions and take meaningful steps to enhance their risk profiles,” Sherron explained.

She encourages agents to engage in open and honest dialogue with clients affected by cancellation, non-renewal, or declination of coverage.

“Make it clear that carriers are legally required to provide reasons for adverse actions, and how this helps both parties work together to address concerns and identify the best strategy and solution moving forward,” Sherron said.

How to interpret carrier responses

When reviewing carrier responses from insurance companies, both agents and clients should carefully examine the reasons provided and ask clarifying questions if there is any confusion or uncertainty.

“Agents should be prepared to discuss carrier expectations and underwriting guidelines to provide context and help clients better understand their own risk profiles. It’s also their responsibility to guide clients on steps they can take to improve their eligibility for coverage,” Sherron explained.

At the end of the day, maintaining proactive and ongoing dialogue between agents and clients about issues that could lead to declination, cancellation, or non-renewal of coverage is critical to avoiding surprises, experts say.

Factors such as outstanding carrier requirements for a home, increased auto activity, or a pattern of frequent claims can trigger adverse carrier actions if left unaddressed.

“An annual review of the insurance program is an excellent opportunity to assess potential issues and discuss changes that may reduce the likelihood of future carrier actions,” Sherron added.

Much attention has focused on the more than 4 million baby boomers turning 65 each year, often referred to as “Peak 65.” Today, as many Americans are turning 35 as are turning 65, marking “Peak 35.”

Millennials are emerging as the next financial phenomenon — already shaping the economy through entrepreneurship, professional success, strategic real estate acquisitions, and willingness to consider alternative investments. Many have built wealth at a younger age than previous generations, while others face financial pressures like student debt and wage stagnation.

These millennials are a driving force in the American economy as the largest generation in the workforce. As they transition from early career earnings to wealth building, many are also poised to inherit assets from their baby boomer parents.

A new study by Equitable, “PEAK 35TM: Guiding a New Generation of Wealth, explores how millennials are both building and inheriting wealth.

The study reveals that nearly seven in 10 millennials expect or are fairly confident they will inherit assets from their families. They anticipate receiving a range of wealth, including cash (71%), personal valuables such as jewelry (51%), real estate assets (46%), and transfer of financial assets like stocks, bonds and retirement accounts (41%).

Nearly eight in 10 millennials feel confident making smart financial decisions today; that confidence drops sharply to just 27% when their financial situation becomes more complex. As millennials prepare to inherit cash, real estate, investments and businesses from their aging parents, this shift in assets presents an opportunity for advisors to offer expert guidance and holistic financial planning.

“I was surprised at how confident millennials are with their finances,” said Michelle Felendes, a financial advisor with Equitable Advisors. “Of course, that confidence drops when things get tricky. For example, when their parents pass away and there is a transfer of wealth.”

Navigating personal financial planning landscapes, including tax laws, while raising children and dealing with your parents can be complicated, Felendes noted. “It’s not just the numbers; it’s the human side of life.”

Female millennials are a growing financial influence

Millennial women are another critical demographic in today’s financial landscape, with growing influence over personal and family wealth. Their financial circumstances are increasingly complex as they balance career advancement, caregiving responsibilities and potential wealth transfer considerations.

More millennial women are advancing in their careers, with higher education and larger incomes positioning them to take control of their financial futures. Fifty-one percent of millennial women report that they are the primary breadwinners in their families — surpassing both Gen X (39%) and baby boomer women (37%) in this role.

Single women are outpacing men in home ownership, highlighting their financial independence and need for long-term planning.

Despite millennial women’s growing economic power, there is a gender divide in confidence managing their finances today, the study found.

Eighty-five percent of men feel confident in their ability to make smart financial decisions today versus just 71% of women. The study reveals that having a financial advisor, however, increases confidence levels among millennial women to 84%.

When it comes to finances and investments, Felendes said many women historically relegate that to their male counterparts, but she is seeing many millennial women taking more of an active role.

Digital natives are looking for human advice

As the first digital-native generation, millennials embrace technology, social media and mobile finance. While digital finance tools provide convenience, millennials seek personalized financial guidance as they build and inherit wealth.

Importantly, nearly seven in 10 millennials (68%) would prioritize working with a financial advisor over a solely digital experience. The study shows that 27% of millennials prefer working just with a financial advisor, while 41% favor a hybrid approach that balances technology and tailored advice.

“Having an advisor can help people reach their goals. I always tell my clients, ‘My goal is to help make your life easier.’ There is a lot of information out there but how do you take that information and execute on it,” Felendes said.

The study reveals that 68% of millennials have already discussed future inheritance planning with their parents, and two-thirds of those families work with a financial advisor — underscoring that financial planning often begins at home.

That influence runs deep: 87% of millennials say their family’s relationship with a financial advisor is a key factor in deciding whether to continue working with that advisor themselves. Four in 10 millennials, however, would switch financial advisors if they do not feel seen or supported, or if the advisor lacks experience with clients in a similar situation.

Felendes recommends that millennials meet with a financial professional with their parents. This can give clarity on their own planning because she says, “You don’t know what you don’t know.”

The current shift in wealth is more than a financial decision for most millennials — it’s emotional and cultural. The study revealed that an overwhelming 93% of millennials believe it’s important for their financial advisor to align with their personal values and goals. Moreover, nearly three-quarters of those already working with a financial advisor plan to seek one who specializes in inheritance and wealth transfer.

Equitable’s “PEAK 35TM: Guiding a New Generation of Wealth” study was conducted by an independent, global survey panel provider. The survey included 500 U.S. adults born between 1981 and 1996 and was fielded online between June 26 and July 7, 2025.