Annuity sales edge up in Q3, Wink reports

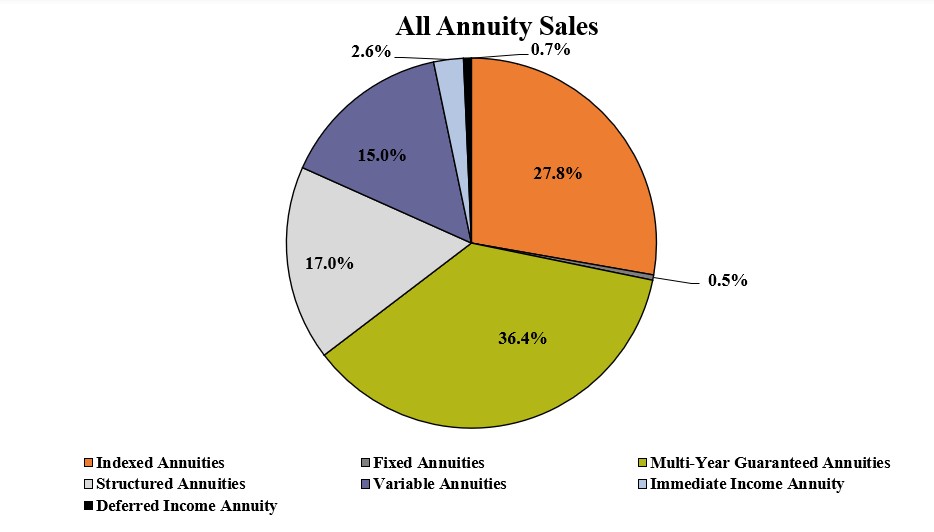

Total third-quarter sales for all annuities were $117.0 billion, Wink’s Sales and Market Report said. Sales were up 1.8% when compared to the previous quarter and up 1.5% when compared to the same period last year.

Annuities tracked in the report include the multiyear guaranteed annuity, traditional fixed annuity, indexed annuity, structured annuity, variable annuity, immediate income annuity and deferred income annuity product lines.

Noteworthy highlights for all annuity sales in the third quarter include Athene USA ranking as the No. 1 carrier overall for annuity sales, with a market share of 9.1%. Nationwide came in second place, while Jackson National Life, Corebridge Financial and New York Life completed the top five carriers in the market, respectively.

Total third quarter sales for all deferred annuities were $113.2 billion; sales were up 1.4% when compared to the previous quarter and up 2.0% when compared to the same period last year. Since Wink began tracking sales, this was a record-setting quarter for deferred annuity sales, topping the prior 2nd quarter 2025 record by 1.4%. All deferred annuities include the multiyear guaranteed annuity, traditional fixed, indexed annuity, structured annuity, and variable annuity product lines.

Noteworthy highlights for all deferred annuity sales in the third quarter include Athene USA ranking as the No.1 carrier overall for deferred annuity sales, with a market share of 9.4%. Nationwide moved into the second-ranked position, while Jackson National Life, Corebridge Financial, and Allianz Life completed the top five carriers in the market, respectively. Nationwide’s Nationwide Secure Growth 5-Year, a MYG annuity, was the #1 selling deferred annuity, for all channels combined, for the quarter.

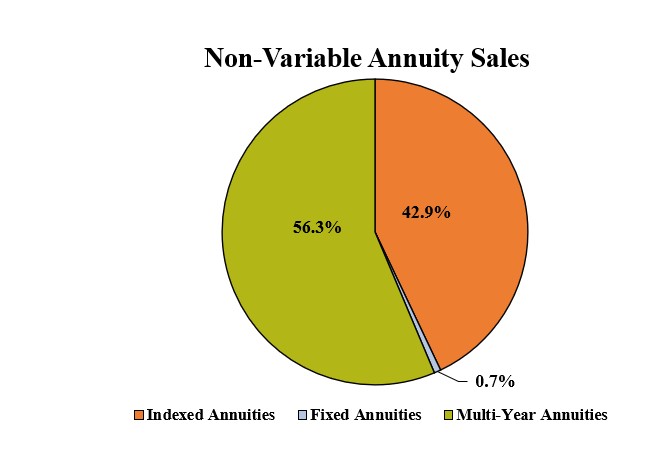

Total third quarter non-variable deferred annuity sales were $75.6 billion; sales were down 2.9% when compared to the previous quarter and down 5.1% when compared to the same period last year. Non-variable deferred annuities include the MYG annuity, traditional fixed annuity, and indexed annuity product lines.

Noteworthy highlights for non-variable deferred annuity sales in the third quarter include Athene USA ranking as the No. 1 carrier overall for non-variable deferred annuity sales, with a market share of 13.5%. Corebridge Financial took the second-ranked position, while Nationwide, Massachusetts Mutual Life Companies and Allianz Life completed the top five carriers in the market, respectively. Nationwide’s Nationwide Secure Growth 5-Year, a MYG annuity, was the #1 selling non-variable deferred annuity, for all channels combined, for the quarter.

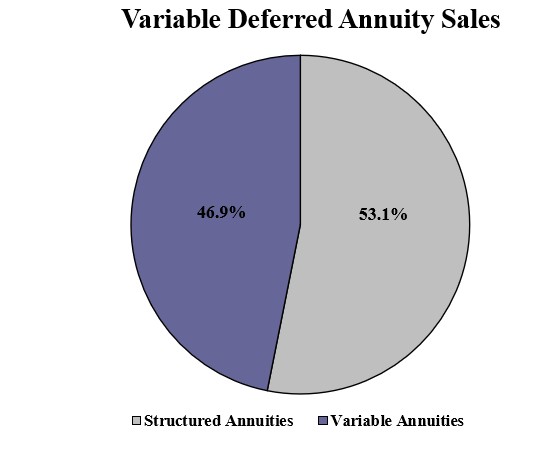

Total third quarter variable deferred annuity sales were $37.5 billion; sales were up 11.7% when compared to the previous quarter and up 20.3% when compared to the same period last year. Variable deferred annuities include structured annuity and variable annuity product lines.

Noteworthy highlights for variable deferred annuity sales in the third quarter include Jackson National Life ranking as the No. 1 carrier overall for variable deferred annuity sales, with a market share of 16.1%. Equitable Financial moved into the second-place position, as Lincoln National Life, Allianz Life, and Brighthouse Financial completed the top five carriers in the market, respectively. Jackson National’s Perspective II Flexible Premium Variable & Fixed Deferred Annuity, a variable annuity, was the No. 1 selling variable deferred annuity, for all channels combined, for the quarter.

Total third quarter income annuity sales were $3.8 billion; sales were up 15.3% when compared to the previous quarter and down 10.7% when compared to the same period last year. Income annuities include immediate income annuity and deferred income annuity product lines.

Noteworthy highlights for income annuity sales in the third quarter include New York Life ranking as the No. 1 carrier overall for income annuity sales, with a market share of 41.0%. Massachusetts Mutual Life Companies continued in the second-ranked position, as USAA, Nationwide, and Western-Southern Life Assurance Company completed the top five carriers in the market, respectively.

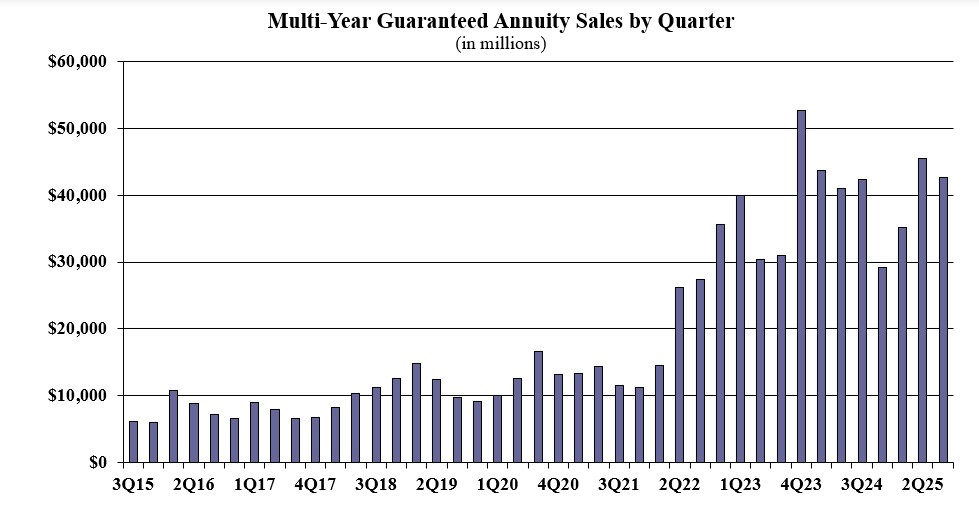

Multiyear guaranteed annuity sales in the third quarter were $42.6 billion; sales were down 6.1% when compared to the previous quarter, and up 0.5% when compared to the same period, last year. MYGAs have a fixed rate that is guaranteed for more than one year.

Noteworthy highlights for MYGAs in the third quarter include Athene USA ranking as the No. 1 seller, with a market share of 14.0%. Nationwide continued in the second-ranked position, while Massachusetts Mutual Life Companies, New York Life, and Corebridge Financial concluded as the top five carriers in the market, respectively. Nationwide’s Nationwide Secure Growth 5-Year product was the No. 1 selling multi-year guaranteed annuity, for all channels combined, for the quarter.

Traditional fixed annuity sales in the third quarter were $538.0 million; sales were up 15.9% when compared to the previous quarter, and up 4.1% when compared with the same period last year. Traditional fixed annuities have a fixed rate that is guaranteed for one year only.

Noteworthy highlights for traditional fixed annuities in the third quarter include Global Atlantic Financial Group ranking as the No. 1 seller, with a market share of 16.2%. Nationwide ranked second, while Equitable Financial, CNO Companies, and National Life Group concluded as the top five carriers in the market, respectively. Forethought Life’s ForeCare Fixed Annuity was the No. 1 selling fixed annuity, for all channels combined, for the twenty-first consecutive quarter.

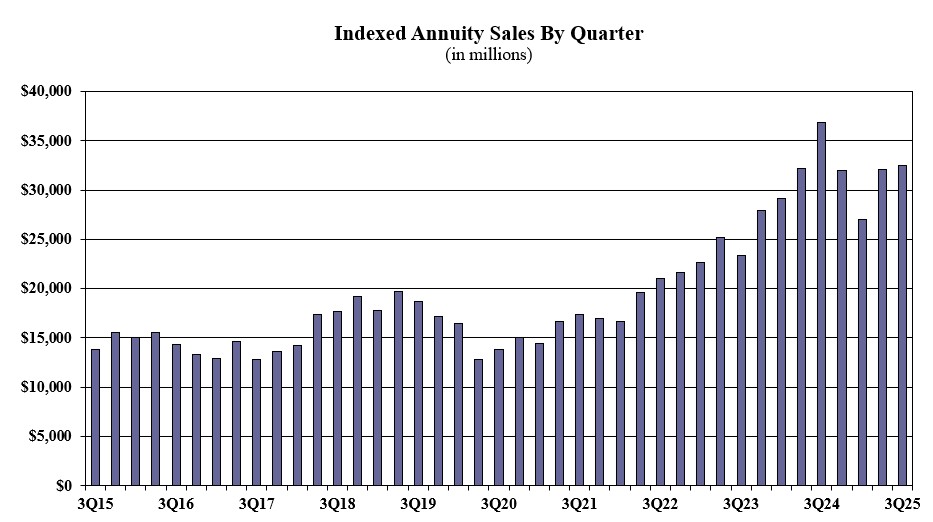

Indexed annuity sales for the third quarter were $32.4 billion; sales were up 1.2% when compared to the previous quarter, and down 11.7% when compared with the same period last year. Indexed annuities have a floor of no less than zero percent and limited excess interest that is determined by the performance of an external index, such as Standard and Poor’s 500®.

Noteworthy highlights for indexed annuities in the third quarter include Athene USA ranking as the No. 1 seller, with a market share of 13.0%. Allianz Life ranked second, while Corebridge Financial, American Equity Companies, and Sammons Financial Companies completed the top five carriers in the market, respectively. Athene’s Athene Ascent Pro 10 was the No. 1 selling indexed annuity, for all channels combined, for the quarter.

Sheryl Moore, CEO of both Wink, Inc., and Moore Market Intelligence commented, “The innovation that I am seeing in the indexed annuity market is incredible. I project that these products will become even more consumer friendly, as sales of these products increase.”

Structured annuity sales in the third quarter were $19.9 billion; sales were up 9.5% as compared to the previous quarter, and up 23.9% as compared to the same period last year. It was a record-setting quarter for structured annuity sales; topping the prior 2nd quarter 2025 record by 9.5%. Structured annuities have a limited negative floor and limited excess interest that is determined by the performance of an external index or subaccounts.

Noteworthy highlights for structured annuities in the third quarter include Equitable Financial ranking as the No. 1 seller, with a market share of 19.4%. Allianz Life ranked second, while Jackson National Life, Brighthouse Financial, and Prudential completed the top five carriers in the market, respectively. Equitable’s Structured Capital Strategies Plus 21 was the No. 1 selling structured annuity, for all channels combined, for the sixth consecutive quarter.

“The carrier I mentioned in last quarter’s press release is still moving mountains,” declared Moore. “This long-time variable annuity leader isn’t going to be stopped, until they rank #1 in structured annuities! (And they will hold onto it!)”

Variable annuity sales in the third quarter were $17.5 billion; sales were up 14.3% as compared to the previous quarter, and up 16.5% compared to the same period last year. Variable annuities have no floor, and the potential for gains/losses is determined by the performance of subaccounts that may be invested in an external index, stocks, bonds, commodities, or other investments.

Noteworthy highlights for variable annuities in the third quarter include Jackson National Life ranking as the No. 1 seller, with a market share of 22.6%. Nationwide ranked second, while Equitable Financial, Lincoln National Life, and New York Life finished as the top five carriers in the market, respectively. Jackson National’s Perspective II Flexible Premium Variable & Fixed Deferred Annuity was the No. 1 selling variable annuity for the twenty-sixth consecutive quarter, for all channels combined.

Immediate income annuity (Single Premium Immediate Annuity, a.k.a. SPIA) sales in the third quarter were $3.0 billion; sales were up 15.5% as compared to the previous quarter and down 2.0% as compared to the same period last year.

Noteworthy highlights for SPIAs in the third quarter include New York Life ranking as the No. 1 seller, with a market share of 42.6%. Massachusetts Mutual Life Companies ranked second, while USAA, Nationwide, and Western-Southern Life Assurance Company finished as the top five carriers in the market, respectively.

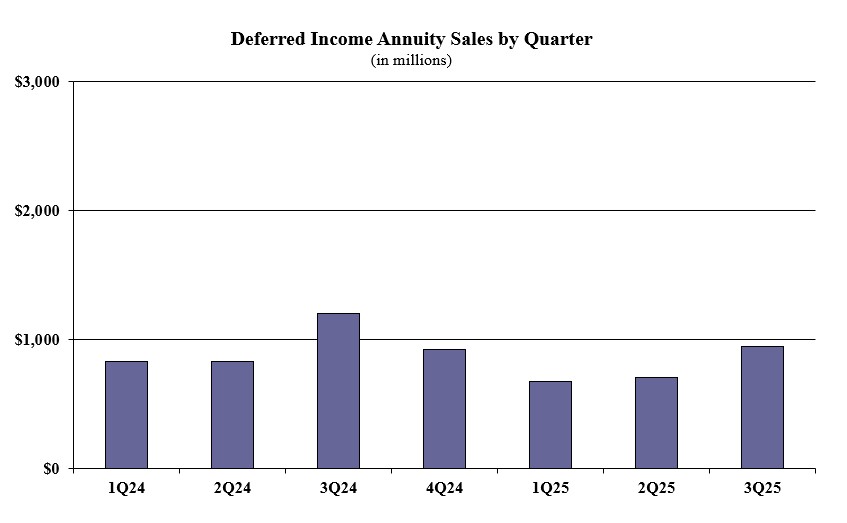

Deferred income annuity sales in the third quarter were $945.8 million; sales were up 34.8% compared to the previous quarter and down 21.2% as compared to the same period last year.

Noteworthy highlights for DIAs in the third quarter include New York Life ranking as the No. 1 seller, with a market share of 29.7%. Massachusetts Mutual Life Companies ranked second, as USAA, Western-Southern Life Assurance Company, and Integrity Life Companies finished as the top five carriers in the market, respectively.

The post Annuity sales edge up in Q3, Wink reports appeared first on Insurance News | InsuranceNewsNet.